Is Equity Release Safe? Debunking Retirement Myths

Equity release is safe when chosen carefully, thanks to regulations and protections like the no negative equity guarantee. We consider informed decision-making crucial for safety.

Last Updated: 24 Apr 2025

Fact Checked

Our team recently fact checked this article for accuracy. However, things do change, so please do your own research.

Katherine Read is a financial writer known for her work on financial planning and retirement finance, covering equity release, lifetime mortgages, home reversion, retirement planning, SIPPs, pension drawdown, and interest-only mortgages.

Bert Hofhuis Is a Founder & Entrepreneur Simplifying the Complexities of Later Life Planning. He Navigates the Intricacies of Equity Release, Lifetime Mortgages, Reverse Mortgages, and Wealth Management With Clarity and Expertise.

In his long professional career, Bert has worked with multinational companies and governments, consulting on various financial and logistical projects in Africa, Europe and Asia.

He founded The Enquirer with a team of experienced finance writers and experts to help demystify topics such as equity release, lifetime mortgages, home reversions and retirement interest only mortgages, for people like himself.

Paul Derek Sawyer is an esteemed external compliance consultant in equity release, specializing in lifetime mortgages and home reversion plans. With over 20 years of experience, he expertly navigates the complexities of Equity Release Council standards and regulations.

His focus is on ensuring ethical lending practices and safeguarding consumer interests. Renowned for his expertise in financial services compliance, risk management, and audit, Paul is dedicated to promoting financial security for the elderly.

Bert Hofhuis Is a Founder & Entrepreneur Simplifying the Complexities of Later Life Planning. He Navigates the Intricacies of Equity Release, Lifetime Mortgages, Reverse Mortgages, and Wealth Management With Clarity and Expertise.

In his long professional career, Bert has worked with multinational companies and governments, consulting on various financial and logistical projects in Africa, Europe and Asia.

He founded The Enquirer with a team of experienced finance writers and experts to help demystify topics such as equity release, lifetime mortgages, home reversions and retirement interest only mortgages, for people like himself.

TheEnquirer Promise

Expert Verified

Assessing Equity Safety: Explore the Safeguards, Risks & Regulatory Measures. But Is It Truly Risk-Free?

Key Takeaways

Safeguards include the "no negative equity guarantee," advice from a qualified adviser, and clear terms regarding fees and interest rates to protect customers.

The no negative equity guarantee ensures that you or your estate will never owe more than the value of your home when it is sold, even if the debt exceeds the property value.

The Equity Release Council sets standards for product providers, ensuring products are safe and transparent, and includes protections like the no negative equity guarantee.

You cannot lose your home as long as you comply with the terms of the agreement, such as maintaining the property and not breaching contract conditions.

Common concerns about equity release safety, like high interest rates and impacting inheritance, are addressed through regulations, the no negative equity guarantee, and the requirement for professional advice.

‘Is equity release safe?’ is a question echoing in the minds of many UK homeowners considering tapping into their property's value.

This financial solution offers a promise of capital without selling one's home, yet it's accompanied by intricate details and potential pitfalls.

As with any substantial financial decision, understanding the nuances, regulations, and potential repercussions is paramount.

What You'll Learn in This Article:

This article delves into the mechanics, benefits, and concerns surrounding these products, aiming to shed light on its safety and suitability for various circumstances.

Here’s a breakdown.

Who Offers the Lowest Rates in 2025?

Discover the Lowest Rates & Save

Request a FREE call back & discover:

Who offers the LOWEST rates available on the market.

It's an industry body dedicated to the advocacy and regulation of the equity release sector, working closely with providers, regulators, and policymakers.

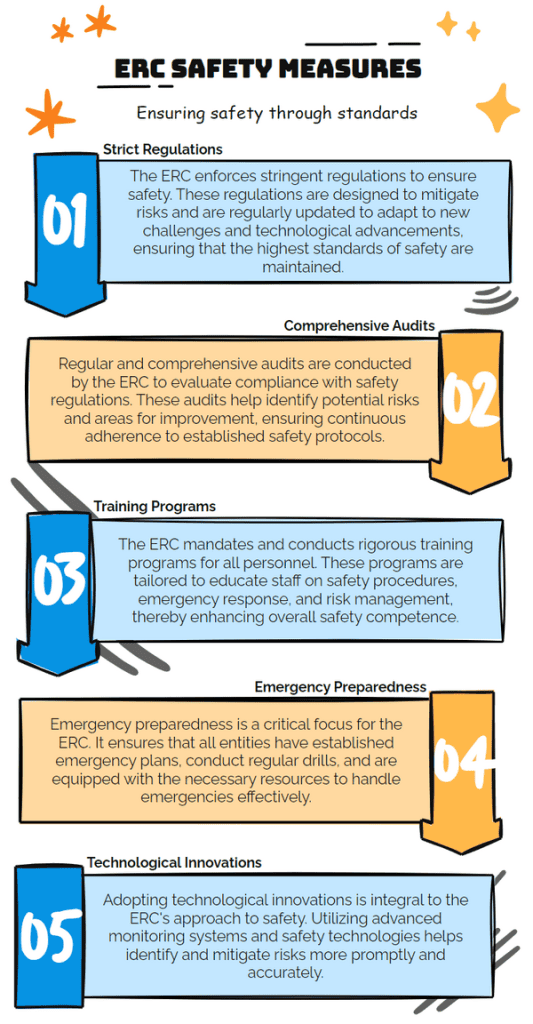

How Does the ERC Ensure Safety?

The ERC ensures safety by enforcing high standards of conduct among its members, and it's these stringent measures that ensures you’ll be protected.

All member firms must adhere to the ERC’s Statement of Principles, which places the consumer's welfare at the heart of all their actions.

Ultimately

These principles stress transparent, fair treatment, and comprehensive financial advice to ensure that consumers make informed decisions.

These include the No Negative Equity Guarantee, ensuring homeowners never owe more than their home's value, and the right to remain in their property for life or until they need to move into long-term care.

Additionally, customers must be advised by a qualified and experienced adviser or broker who has passed specialist examinations.

They ensure that all products are transparent, fair, and sold by competent and qualified individuals.

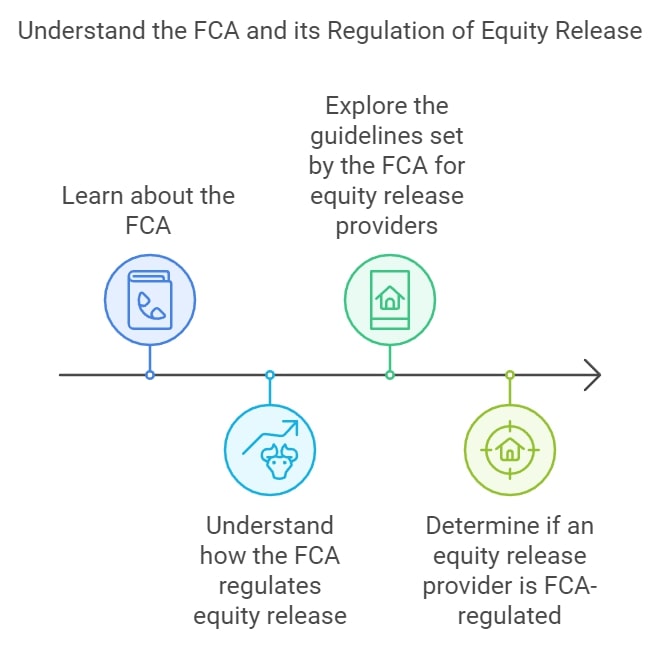

The FCA regularly reviews firms to ensure compliance and can enforce penalties or sanctions for non-compliance.

Guidelines the FCA Set for Equity Release Providers

Some of the key guidelines set by the FCA for providers include providing clear and comprehensible information to consumers, advising them on the potential impacts on their tax position and welfare benefits, and offering an accurate comparison of products available in the market.

How to Determine Whether an Equity Release Provider is FCA-Regulated

Before entering into an agreement with a provider, it's important to verify their FCA registration.

You can do this by checking the Financial Services Register on the FCA’s website.3

This register provides a comprehensive list of all regulated firms and can help you verify that your provider is FCA-regulated and compliant.

Mis-Sold Equity Release Finance

Mis-selling happens when a product, such as a lifetime mortgage or a home reversion plan, is sold to a consumer who doesn't fully understand the implications or for whom the product isn't suitable.

This can lead to unexpected financial problems, including significant debt or even the loss of the home.

How Equity Release is Mis-Sold

Equity release might be mis-sold if a financial advisor fails to provide clear and comprehensive information about the product and its potential risks.

It might also occur if they don't consider your financial situation, needs, or the potential impact of the equity release on your benefits or taxes.

If they rush you into making a decision without giving you time to consider alternatives, this could also be a case of mis-selling.

What to Watch Out For with Mis-Selling

Mis-selling signs include advisors not explaining the downsides of equity release, not exploring other financial options, or not making it clear that releasing equity could affect your tax status or benefits.

Be wary of high-pressure sales tactics, such as urgency to sign documents without sufficient time to understand them fully.

What to Do if You’ve Been Mis-Sold

If you believe you've been mis-sold a product, you should first lodge a complaint with the company that sold it to you.

If they don't resolve your complaint satisfactorily, you can take your complaint to the Financial Ombudsman Service (FOS),4 an independent body that settles disputes between consumers and financial businesses.

Retirement Financial Advice Other Organisations

Reliable and impartial retirement financial advice is available from many other organisations.

They can help you understand the implications of equity release and other financial products.

Organisations That Offer Retirement Financial Advice

Several organisations can provide advice, such as the Money and Pensions Service (MaPS),5 Age UK,6 and Citizens Advice.7

These bodies offer free, impartial advice to help you make informed decisions about your financial future.

Finding Reputable Financial Advice Providers in the UK

When seeking advice, always ensure the provider is regulated by the FCA.

You can check this on the FCA's Financial Services Register.

Also, consider if they have specialist qualifications in equity release and are members of reputable bodies, such as the Equity Release Council.

Why You Should Seek Professional Advice

Seeking professional advice is essential since a reputable advisor will take time to understand your situation, explain the potential impacts of equity release, and help you explore all available options.

Also

They will ensure that you make an informed decision that suits your financial circumstances and future needs.

Common Questions

Does Equity Release Have Risks?

Yes, like any financial product, equity release does carry certain risks.

These include the possibility of accruing more debt than anticipated due to the compounding of interest, reducing your ability to leave an inheritance, and potentially affecting your eligibility for means-tested benefits.

It's crucial to consider these potential risks and discuss them with a financial advisor before deciding on equity release.

How Do You Tell If Equity Release Is Right for You?

Determining whether equity release is right for you involves considering your financial situation, future needs, and goals.

Questions to consider include:

Do you need a cash lump sum or additional regular income?

Are you comfortable with the impact on the amount you can leave as an inheritance?

These are complex considerations, and professional advice is crucial to making an informed decision.

What Happens to Your Property When You Pass Away?

Upon your death or if you move into long-term care, the equity release provider will sell your home to repay the loan and any accrued interest.

If there is any money left after the sale, it will go to your estate.

If you have a joint plan and one of you passes away, the other can continue living in the property under the same terms.

How Long Is the Entire Equity Release Process?

The process typically takes between 6 to 12 weeks from the moment you apply to when you receive the funds.

This timeframe can vary depending on your provider, the complexity of your situation, and how quickly your solicitor can work through the legal process.

How Much Can You Get From Equity Release?

The amount you can release from your home depends on various factors, including your age, the value of your property, and the specific plan you choose.

Typically, you can borrow up to 60% of your home's value, but this can be higher or lower depending on the circumstances.

An equity release calculator can provide an estimate, but a professional advisor will give a more accurate figure.

Can You Still Leave an Inheritance With Equity Release?

Yes, it's still possible to leave an inheritance, but it will likely be smaller.

Some plans allow you to ring-fence a portion of your property's value as a guaranteed inheritance.

However

Because equity release reduces the value of your estate, the inheritance you leave could be significantly less than if you hadn't released equity.

In Conclusion

Equity release in the UK can provide substantial benefits for homeowners over 55.

However, it's crucial to fully understand the process, potential risks, and benefits, keeping in mind the potential for mis-selling.

The Equity Release Council and the Financial Conduct Authority work to ensure the safety of these schemes.

Remember, a significant financial decision demands careful consideration and thorough research.

Before proceeding, always verify your provider's credibility and seek professional, impartial advice to determine whether equity release is safe or not.

Editorial Note: This content has been independently collected by the SovereignBoss team and is offered on a non-advised basis. SovereignBoss may earn a commission on sales made from partner links on this page, but that doesn’t affect our editors’ opinions or evaluations. Learn more about our editorial guidelines.

How Does TheEnquirer Ensure Expert-Verified Content?

At TheEnquirer, the integrity and precision of our information is paramount.

Being "expert verified" signifies that our review panel has meticulously assessed each article for precision and comprehensibility. This panel is made up of seasoned professionals in compliance is dedicated to guaranteeing that our content remains impartial and well-informed.

Their rigorous evaluations compel us to maintain a standard of excellence, ensuring that the information we provide is both reliable and of the highest quality.

Financial Guidance Disclaimer for TheEnquirer Readers

Understanding Our Revenue Stream

TheEnquirer operates as an autonomous, ad-supported online platform. Our mission is to furnish you with essential tools and insights for wiser financial choices, granting access to our interactive resources and impartial journalism at no cost.

Please note that while our content is educational, it is not meant as specific financial advice and should not be the only factor in your decision-making. We advise seeking personalized advice from a financial expert to cater to your unique investment needs.

How We Generate Income

Our earnings come from endorsements for products featured on our website. This financial relationship might influence how products are displayed, yet it does not impact the integrity and thoroughness of our information and evaluations. Note that we do not encompass every available financial product or offer.

Commitment to Editorial Integrity

Our reviews are exclusively authored by our editorial staff, reflecting their own views. These insights remain unswayed by our sponsors. At TheEnquirer, we adhere to stringent principles of editorial independence and fairness to ensure unbiased content..

Expert Verified

Expert Verified

How Does TheEnquirer Ensure Expert-Verified Content?

How Does TheEnquirer Ensure Expert-Verified Content?