You can get equity release if you still have a mortgage, but the equity release funds must first be used to pay off the existing mortgage. We find this stipulation crucial for eligibility.

Last Updated: 22 Apr 2025

Fact Checked

Our team recently fact checked this article for accuracy. However, things do change, so please do your own research.

Katherine Read is a financial writer known for her work on financial planning and retirement finance, covering equity release, lifetime mortgages, home reversion, retirement planning, SIPPs, pension drawdown, and interest-only mortgages.

Bert Hofhuis Is a Founder & Entrepreneur Simplifying the Complexities of Later Life Planning. He Navigates the Intricacies of Equity Release, Lifetime Mortgages, Reverse Mortgages, and Wealth Management With Clarity and Expertise.

In his long professional career, Bert has worked with multinational companies and governments, consulting on various financial and logistical projects in Africa, Europe and Asia.

He founded The Enquirer with a team of experienced finance writers and experts to help demystify topics such as equity release, lifetime mortgages, home reversions and retirement interest only mortgages, for people like himself.

Paul Derek Sawyer is an esteemed external compliance consultant in equity release, specializing in lifetime mortgages and home reversion plans. With over 20 years of experience, he expertly navigates the complexities of Equity Release Council standards and regulations.

His focus is on ensuring ethical lending practices and safeguarding consumer interests. Renowned for his expertise in financial services compliance, risk management, and audit, Paul is dedicated to promoting financial security for the elderly.

Bert Hofhuis Is a Founder & Entrepreneur Simplifying the Complexities of Later Life Planning. He Navigates the Intricacies of Equity Release, Lifetime Mortgages, Reverse Mortgages, and Wealth Management With Clarity and Expertise.

In his long professional career, Bert has worked with multinational companies and governments, consulting on various financial and logistical projects in Africa, Europe and Asia.

He founded The Enquirer with a team of experienced finance writers and experts to help demystify topics such as equity release, lifetime mortgages, home reversions and retirement interest only mortgages, for people like himself.

TheEnquirer Promise

Expert Verified

Explore the Intricacies of Combining Equity Release and Mortgages. Uncover the Opportunities and Challenges, & Understand How It Reshapes Your Financial Landscape. Dive Into UK’s Equity Release Insights!

Key Takeaways

You can get equity release even if you still have a mortgage, but the funds must first be used to pay off the existing mortgage.

Having a mortgage affects your options by reducing the amount of equity available to release, as the initial lump sum must cover the remaining mortgage balance.

When you take out a plan, your existing mortgage is paid off with the proceeds from the plan, and any remaining funds are provided to you.

It can indeed be used to pay off a mortgage, allowing homeowners to remain in their homes mortgage-free, though it's important to consider the long-term implications on inheritance and interest accumulation.

While there are no specific plans exclusively for people with mortgages, many plans are designed with flexibility to accommodate borrowers who need to pay off an existing mortgage as part of the process.

Considering tapping into your property's value using equity release with an existing mortgage in the UK?

However, as with many financial instruments, it has its intricacies, opportunities, and challenges.

What You'll Learn in This Article:

From understanding overlapping costs to the implications on future refinancing and inheritance, this article delves into the multifaceted realm of merging equity release and mortgages, shedding light on the benefits and potential pitfalls that lie ahead.

Who Offers the Lowest Rates in 2025?

Discover the Lowest Rates & Save

Request a FREE call back & discover:

Who offers the LOWEST rates available on the market.

Can You Take Out Equity Release With an Existing Mortgage?

Yes, you can take out equity release if you have an existing mortgage, but the funds obtained must first be used to pay off the existing mortgage balance.

It's essential to seek professional advice to fully understand the implications and terms.

What’s the Feasibility of Equity Release with a Mortgage?

The feasibility of equity release with a mortgage depends on a few factors including the amount in your outstanding mortgage, LTV ratio, and interest rates.

Here’s a more detailed breakdown:

Outstanding Mortgage: Schemes require that any existing mortgage on the property be repaid either before taking out the equity release or from the proceeds of the loan. If the equity you intend to release is less than the outstanding mortgage, it won’t be feasible option.

Loan-to-Value (LTV) Ratio: Providers have a maximum loan-to-value ratio, which determines how much you can borrow against the value of your home. Remember, since you already have a mortgage, the amount you can release will also be reduced by whatever is outstanding.

Interest Rates: These can be higher than traditional mortgages. Over time, the rolled-up interest can significantly reduce the remaining equity in your home, which can affect inheritance planning.

Future Flexibility: Consider the flexibility you might need in the future. Some schemes may limit your ability to move or downsize.

Costs: Including arrangement fees, valuation fees, solicitor fees, and possibly advisor fees.1 Make sure you understand all the costs upfront.

Alternatives: Before settling, consider other options to raise funds, like downsizing, using savings, or borrowing from family.

Criteria & Conditions for Applying

There are specific criteria and conditions that you must meet to be eligible for equity release, especially with an existing mortgage, which relate to age, your property, and your current mortgage amount.

Here are some of the typical criteria and conditions:

Age Requirement: The youngest homeowner (whether a single or joint applicant) must be at least 55 years old.

Property Value:The equity release provider sets the minimum property value, usually starting at around £70,000.2

Existing Mortgage Amount: The outstanding amount on your mortgage will directly impact the amount you can borrow. Therefore, the equity release sum should cover the existing mortgage.

Property Location and Condition: Your property should be in the UK and maintained to a standard acceptable to the provider.

Professional Advice: It's a requirement by the Equity Release Council that anyone considering equity release consults with a qualified financial adviser to understand the potential implications fully.

How Does an Outstanding Mortgage Amount Affect Equity Release?

Your home's equity is its current market value minus any debts secured against it, including your mortgage.

The outstanding mortgage amount plays a pivotal role in determining the amount of funds you can release:

Reduction in Available Equity: The amount left on your mortgage directly reduces the equity you can access. If you have a large mortgage, you may need more than the released funds after paying off the mortgage.

Interest Accumulation: Like a traditional mortgage, equity release plans accumulate interest. If you’re taking equity release to pay off a mortgage, you’re essentially replacing one debt with another, which will also accrue interest over time.

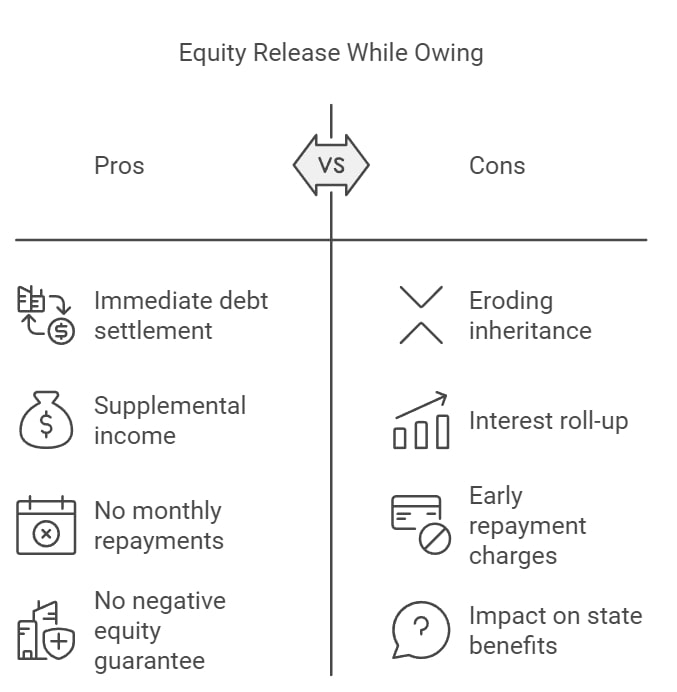

What Are the Pros & Cons of Pursuing Equity Release While Owing?

Immediate Debt Settlement: Equity release may provide the funds necessary to pay off an existing mortgage, eliminating monthly mortgage repayments and easing financial burden.

Supplemental Income: After clearing your mortgage, any additional funds can serve as supplementary income, assisting with retirement expenses or other financial needs.

No Monthly Repayments: Unlike traditional mortgages, equity release plans, such as lifetime mortgages, don’t require monthly repayments, with the loan being repaid after your death, selling, or moving into long-term care.

Eroding Inheritance: The estate's value left to your heirs may be reduced due to the accumulated interest on the equity release loan.

Interest Roll-up: As interest accumulates over time without monthly repayments, the overall debt can grow, resulting in a more significant sum owed when the plan concludes.

Early Repayment Charges: There may be hefty charges if you decide to repay the loan earlier than agreed upon.

Effect on State Benefits: The influx of cash may impact eligibility for means-tested state benefits.

What Are the Financial Implications & Considerations of Equity Release With a Mortgage?

Let’s unpack the financial dimensions and implications of an existing mortgage with an equity release plan, including interest, repayments, and the length of the loan term.

Interest Rates, Repayments & Overlapping Costs

Consider these:

Compounded Interest: One of the key features of lifetime mortgage plans is the roll-up of interest. Rather than making monthly repayments, the interest compounds over time, which can significantly increase the amount owed over the long term.

Clearance of Outstanding Mortgage: When acquiring a plan with an existing mortgage, funds from the released equity will first be used to clear the outstanding mortgage, potentially reducing the cash sum available for other purposes.

Overlapping Costs: You should be mindful of any overlapping costs, such as fees associated with ending your existing mortgage and initiating an equity release plan. These include arrangement fees, valuation fees, and potential early repayment charges on your mortgage.

Impact on Future Refinancing & Mortgage Terms

Also, consider the impact on future refinancing and mortgage terms, like:

Limited Refinancing Options: Once you've taken out an equity release plan, your ability to refinance or switch mortgage products in the future may be constrained.

Fixed Lifetime Interest Rates: Plans come with a fixed interest rate for life, ensuring predictability, you should evaluate how these rates compare to potential future mortgage interest rates.

Term Length Implications: Equity release plans, particularly lifetime mortgages, are designed to last for the duration of your life or until you move into long-term care. This can be contrasted with traditional mortgages, which have set terms and may offer more flexibility for changes in the future.

Common Questions

How Does the Outstanding Mortgage Impact My Eligibility?

Your outstanding mortgage will only impact your eligibility negatively if you don’t have enough property equity to pay off your loan.

Are There Early Repayment Charges with Combined Solutions?

Yes, some equity release plans and mortgages may impose early repayment charges if you settle the debt before the agreed-upon term.

But remember, these charges pertain to equity release and traditional mortgage separately, as there’s no combined solution.

How Does Taking Equity Release Affect My Remaining Mortgage Term?

Taking equity release doesn't directly affect your remaining mortgage term, but your existing mortgage will need to be settled from the equity release funds, thus terminating your current mortgage term.

What if My Property’s Value Decreases Over Time?

If your property's value decreases, you may be left in a situation where the value is less than what you owe.

But many equity release plans in the UK offer a No Negative Equity Guarantee, ensuring you won't owe more than the property's worth when it’s time to repay the loan.

Your lender will write off any additional debt.

How Can I Use the Released Equity With an Existing Mortgage?

The released equity must first be used to pay off your existing mortgage, and any surplus can be used as you see fit (as long as it’s legal), from home renovations to supplementing retirement income.

What Are the Tax Implications of Double Financing?

There wouldn’t be tax implications for double financing as you aren’t able to have a traditional mortgage and equity release on the same property simultaneously.

And while the released equity itself is tax-free, it may affect eligibility for means-tested benefits and have implications for inheritance tax.

Are There Special Equity Release Plans for Mortgaged Properties in the UK?

No, there aren't specific "mortgaged property" equity release plans. Many providers offer solutions suitable if you have an existing mortgage, provided the released equity is sufficient to cover the outstanding mortgage.

In Conclusion

Navigating the complexities of taking out equity release with an existing mortgage requires a nuanced understanding of the financial landscape.

You can access the value in your property to pay off debts, enhance retirement income, or address immediate financial needs.

However, this journey is fraught with considerations ranging from interest rates to potential impacts on estate values and refinancing options.

While opportunities abound for enhanced financial flexibility, it's crucial to acknowledge potential pitfalls and engage with expert guidance.

Ultimately, to make an informed decision, you should weigh the pros and cons associated with pursuing equity release with a mortgage.

How Does TheEnquirer Ensure Expert-Verified Content?

At TheEnquirer, the integrity and precision of our information is paramount.

Being "expert verified" signifies that our review panel has meticulously assessed each article for precision and comprehensibility. This panel is made up of seasoned professionals in compliance is dedicated to guaranteeing that our content remains impartial and well-informed.

Their rigorous evaluations compel us to maintain a standard of excellence, ensuring that the information we provide is both reliable and of the highest quality.

Financial Guidance Disclaimer for TheEnquirer Readers

Understanding Our Revenue Stream

TheEnquirer operates as an autonomous, ad-supported online platform. Our mission is to furnish you with essential tools and insights for wiser financial choices, granting access to our interactive resources and impartial journalism at no cost.

Please note that while our content is educational, it is not meant as specific financial advice and should not be the only factor in your decision-making. We advise seeking personalized advice from a financial expert to cater to your unique investment needs.

How We Generate Income

Our earnings come from endorsements for products featured on our website. This financial relationship might influence how products are displayed, yet it does not impact the integrity and thoroughness of our information and evaluations. Note that we do not encompass every available financial product or offer.

Commitment to Editorial Integrity

Our reviews are exclusively authored by our editorial staff, reflecting their own views. These insights remain unswayed by our sponsors. At TheEnquirer, we adhere to stringent principles of editorial independence and fairness to ensure unbiased content..

Expert Verified

Expert Verified

How Does TheEnquirer Ensure Expert-Verified Content?

How Does TheEnquirer Ensure Expert-Verified Content?