Equity Release Process: A Step-by-Step Financial Journey

The equity release process in the UK involves expert consultation, property valuation, application, and legal checks, culminating in releasing funds tied up in your home without needing to move out.

Last Updated: 15 Apr 2025

Fact Checked

Our team recently fact checked this article for accuracy. However, things do change, so please do your own research.

Katherine Read is a financial writer known for her work on financial planning and retirement finance, covering equity release, lifetime mortgages, home reversion, retirement planning, SIPPs, pension drawdown, and interest-only mortgages.

Bert Hofhuis Is a Founder & Entrepreneur Simplifying the Complexities of Later Life Planning. He Navigates the Intricacies of Equity Release, Lifetime Mortgages, Reverse Mortgages, and Wealth Management With Clarity and Expertise.

In his long professional career, Bert has worked with multinational companies and governments, consulting on various financial and logistical projects in Africa, Europe and Asia.

He founded The Enquirer with a team of experienced finance writers and experts to help demystify topics such as equity release, lifetime mortgages, home reversions and retirement interest only mortgages, for people like himself.

Paul Derek Sawyer is an esteemed external compliance consultant in equity release, specializing in lifetime mortgages and home reversion plans. With over 20 years of experience, he expertly navigates the complexities of Equity Release Council standards and regulations.

His focus is on ensuring ethical lending practices and safeguarding consumer interests. Renowned for his expertise in financial services compliance, risk management, and audit, Paul is dedicated to promoting financial security for the elderly.

Bert Hofhuis Is a Founder & Entrepreneur Simplifying the Complexities of Later Life Planning. He Navigates the Intricacies of Equity Release, Lifetime Mortgages, Reverse Mortgages, and Wealth Management With Clarity and Expertise.

In his long professional career, Bert has worked with multinational companies and governments, consulting on various financial and logistical projects in Africa, Europe and Asia.

He founded The Enquirer with a team of experienced finance writers and experts to help demystify topics such as equity release, lifetime mortgages, home reversions and retirement interest only mortgages, for people like himself.

TheEnquirer Promise

Expert Verified

Step-by-Step Equity Journey: Learn the Process, Key Stages & What to Expect. But What Challenges Lie Ahead?

Key Takeaways

The first step in the equity release process is consulting with a qualified financial advisor to ensure it's the right decision for your circumstances.

It typically takes 6 to 8 weeks from the initial consultation to receiving the funds.

Legal advice is crucial, ensuring you understand the agreement's terms and protecting your interests throughout the transaction.

You have a 14-day cooling-off period after signing the agreement during which you can change your mind without facing significant penalties.

Costs include advice fees, application fees, valuation fees, and legal fees, which can vary significantly depending on the provider and plan.

Navigating the equity release process can often seem daunting for homeowners keen on tapping into their property's value.

While the promise of releasing tied-up wealth is appealing, the journey involves multiple steps, each with its own significance.

Every phase requires careful thought and understanding, from initial considerations to finalising the agreement.

What You'll Learn in This Article:

This article offers a clear roadmap of the process, breaking down the stages and highlighting essential checkpoints, ensuring homeowners are well-equipped and informed as they embark on this financial venture.

Let’s get started.

Who Offers the Lowest Rates in 2025?

Discover the Lowest Rates & Save

Request a FREE call back & discover:

Who offers the LOWEST rates available on the market.

Here’s a detailed breakdown of what you need to know about each step.

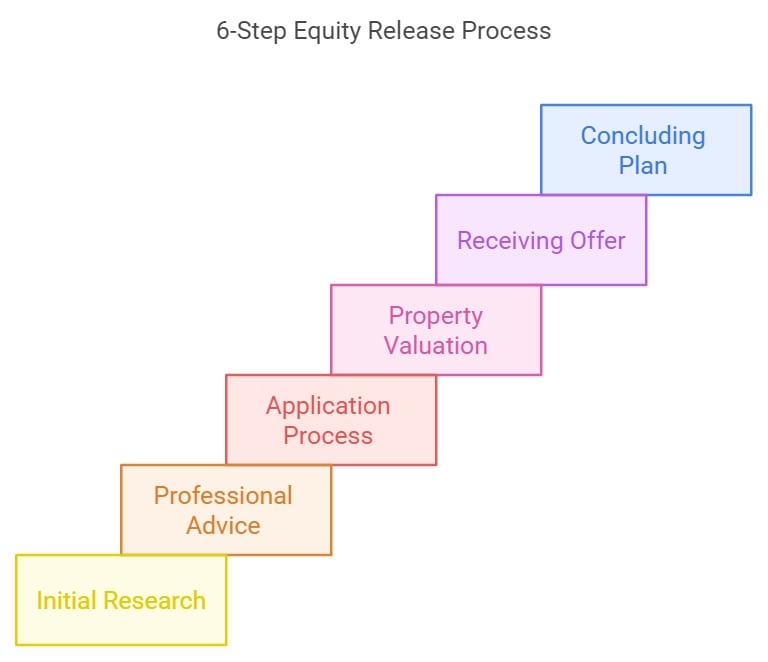

#1. Initial Research

Before diving into equity release, it's crucial to undertake preliminary research to equip yourself with foundational knowledge and tools to better understand the process and its implications.

Consulting an Advisor: Engaging with an expert or specialist in the field ensures that you gather detailed insights, address your pressing questions, and chart a path that aligns with your objectives.

Evaluate the Costs: An advisor's expertise helps decipher the myriad of potential charges, from rolled-up interest rates to application fees, allowing you to grasp the long-term financial ramifications and ensuring full transparency.

#3. The Application Process

Initiating your equity release journey entails a structured application process, laying the groundwork for unlocking the value in your home.

You’ll do so through your chosen lender.

Scheme Selection

Before paperwork begins, understand the 2 main schemes:

Lifetime Mortgages:Borrow against your property's value, repaying the amount when the property is eventually sold.

Home Reversion Plans:Sell part or all of your home to a provider in return for a lump sum or regular payments while residing there.

Documentation

Essential paperwork includes:

Personal details such as age and marital status.

Property specifics, including age and existing mortgages.

Current financial status, detailing debts, assets, and income.

Application Review

Post-submission, the provider evaluates:

The property's aptness for equity release.

The applicant's financial status to ensure mutual feasibility.

Feedback may be requested, and terms could be adjusted based on the provider's assessment.

Conditional Approval

Once aligned, the provider typically grants conditional approval, signalling a positive progression in the process.

The application stage, though methodical, is streamlined when approached with clarity and the right documentation, setting a solid foundation for subsequent phases.

#4. Property Valuation & Surveyor Appointment

Once you decide to proceed, the next step involves a thorough property valuation.

This is achieved by appointing a professional surveyor, typically designated by your provider.

A surveyor will provide:

Objective Assessment: The surveyor's role is to evaluate your property objectively. Their assessment encompasses various facets, from the property's structural integrity and age to its overall condition and unique features.

Market Dynamics: In addition to the physical attributes of the property, external elements, such as the property's geographical location, the desirability of the neighbourhood, and current housing market trends, play a role in its valuation.

#5. Receiving the Offer & Signing the Paperwork

Once the application has been thoroughly evaluated and the property has been valued, the next significant milestone in your journey is the receipt of the offer.

This document is presented by the provider and serves as a formal proposition to the homeowner.

Reviewing the Offer

After a successful application, providers issue an offer outlining the terms, conditions, and the equity release amount.

The offer usually contains:

Terms of Agreement - It describes the specific conditions under which the equity release is proposed.

Release Amount - The document states the exact sum of money that the provider is willing to release based on the home valuation and the homeowner's age.

Interest Rates & Charges - The offer also breaks down the interest rates associated with the equity release and any other fees or charges.

It guarantees that the homeowner is legally protected and that the agreement is transparent, fair, and in line with UK regulations.

Purpose of Representation:

Document Verification - Confirming the authenticity and accuracy of all paperwork.

Legal Counselling - Providing the homeowner with guidance on the legal implications of the agreement.

Liaison with Provider - Acting as a bridge between the homeowner and the provider, ensuring all concerns are addressed.

#6. Concluding the Process & Accessing Your Funds

Once all the necessary checks are conducted, documents are verified, and both parties agree, the process approaches completion.

Accessing the Funds - Upon successfully concluding the process, the funds corresponding to the assessed property value are readied for release.

Continued Residency - One of the main attractions of a lifetime mortgage equity release is the ability to access funds without relinquishing property ownership or residency.

Common Questions

Is the Home Reversion Process the Same as the Lifetime Mortgage Equity Release Process?

No, the Home Reversion process differs from the Lifetime Mortgage Equity Release process.

With a Home Reversion, you sell part or all of your home to a reversion company in return for a lump sum or regular payments, but you can live there rent-free until you die or move out.

With a Lifetime Mortgage, you borrow money against the value of your home while retaining ownership.

Who Can Apply For Equity Release

Individuals who can apply must be 55 or older, own a primary residence in the UK, and meet specific property value and condition requirements.

Eligibility criteria may vary among lenders, so it's best to consult a professional adviser for personalised guidance.

Must You Pay for Equity Release Advisor Services?

Yes, typically, you must pay for advisory services.

These professionals provide valuable advice to help you make informed decisions about the different products, and their fees can be a flat rate, a percentage of the loan amount, or a combination of both.

Costs can vary, however, depending on the complexity of your situation and the advisor you choose.

How Does a Property’s Value Get Assessed for Equity Release?

A property's value is assessed by a professional surveyor who evaluates the property's size, location, condition, age, and the sale prices of similar properties in the area.

This valuation is usually arranged by the lender or provider as part of the application process, and it helps determine the maximum amount of equity that can be released.

Can You Take Out Equity Release if You Still Have a Mortgage?

Yes, you can take out an equity release even if you still have a mortgage.

Any remaining funds can be used at your discretion after paying off the mortgage.

Can You Move or Sell Your Property if You Have an Equity Release Plan?

Yes, you can move or sell your property even if you have a plan, but it may be subject to conditions and potential charges.

For instance

If your provider approves, you might have to repay some or all of the equity you've released or transfer the plan to a new property.

How Long Can It Usually Take to Release Equity From a Property?

Releasing equity from a property typically takes 6 to 12 weeks, but this will depend on your lender and case.

However, the exact timeframe can vary based on the lender's process, property valuation, and applicant's financial circumstances.

Does Age or Health Affect Equity Release Eligibility?

Yes, both age and health can affect equity release eligibility.

Typically, you must be at least 55 to qualify for most lifetime mortgage schemes and 65 for home reversions, and some plans offer more favourable terms for older applicants.

Health can also influence eligibility and terms; some providers may offer enhanced terms if you have certain health conditions.

What Fees & Charges Does Equity Release Have?

Equity release can come with several types of fees and charges, including:

Arrangement or application fees

Valuation fees

Legal fees

Early repayment charges

Adviser's fee

Each provider will have their own set of fees, so it's important to understand these before committing to a plan.

In Conclusion

The equity release process offers a viable financial strategy for homeowners, typically over 55, looking to unlock wealth in their property.

The process, which can take 6 to 12 weeks, involves several steps, from application to property valuation and final legal checks.

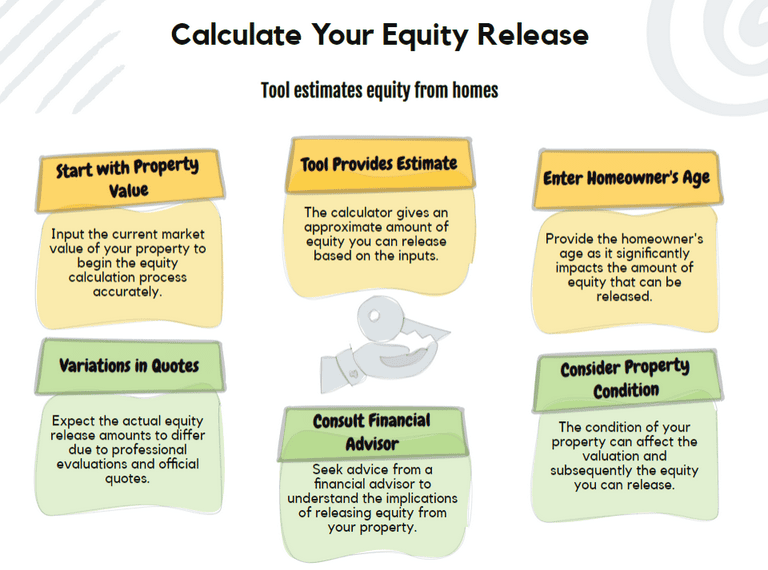

While there are calculator tools to provide estimates, seeking advice from a financial advisor is highly recommended to understand the equity release process fully.

Editorial Note: This content has been independently collected by the SovereignBoss team and is offered on a non-advised basis. SovereignBoss may earn a commission on sales made from partner links on this page, but that doesn’t affect our editors’ opinions or evaluations. Learn more about our editorial guidelines.

How Does TheEnquirer Ensure Expert-Verified Content?

At TheEnquirer, the integrity and precision of our information is paramount.

Being "expert verified" signifies that our review panel has meticulously assessed each article for precision and comprehensibility. This panel is made up of seasoned professionals in compliance is dedicated to guaranteeing that our content remains impartial and well-informed.

Their rigorous evaluations compel us to maintain a standard of excellence, ensuring that the information we provide is both reliable and of the highest quality.

Financial Guidance Disclaimer for TheEnquirer Readers

Understanding Our Revenue Stream

TheEnquirer operates as an autonomous, ad-supported online platform. Our mission is to furnish you with essential tools and insights for wiser financial choices, granting access to our interactive resources and impartial journalism at no cost.

Please note that while our content is educational, it is not meant as specific financial advice and should not be the only factor in your decision-making. We advise seeking personalized advice from a financial expert to cater to your unique investment needs.

How We Generate Income

Our earnings come from endorsements for products featured on our website. This financial relationship might influence how products are displayed, yet it does not impact the integrity and thoroughness of our information and evaluations. Note that we do not encompass every available financial product or offer.

Commitment to Editorial Integrity

Our reviews are exclusively authored by our editorial staff, reflecting their own views. These insights remain unswayed by our sponsors. At TheEnquirer, we adhere to stringent principles of editorial independence and fairness to ensure unbiased content..

Expert Verified

Expert Verified

How Does TheEnquirer Ensure Expert-Verified Content?

How Does TheEnquirer Ensure Expert-Verified Content?