The best source for reliable equity release advice is an independent financial adviser with a specialization in later life lending. We suggest consulting advisers who are members of the Equity Release Council.

Last Updated: 08 Apr 2025

Fact Checked

Our team recently fact checked this article for accuracy. However, things do change, so please do your own research.

Katherine Read is a financial writer known for her work on financial planning and retirement finance, covering equity release, lifetime mortgages, home reversion, retirement planning, SIPPs, pension drawdown, and interest-only mortgages.

Bert Hofhuis Is a Founder & Entrepreneur Simplifying the Complexities of Later Life Planning. He Navigates the Intricacies of Equity Release, Lifetime Mortgages, Reverse Mortgages, and Wealth Management With Clarity and Expertise.

In his long professional career, Bert has worked with multinational companies and governments, consulting on various financial and logistical projects in Africa, Europe and Asia.

He founded The Enquirer with a team of experienced finance writers and experts to help demystify topics such as equity release, lifetime mortgages, home reversions and retirement interest only mortgages, for people like himself.

Paul Derek Sawyer is an esteemed external compliance consultant in equity release, specializing in lifetime mortgages and home reversion plans. With over 20 years of experience, he expertly navigates the complexities of Equity Release Council standards and regulations.

His focus is on ensuring ethical lending practices and safeguarding consumer interests. Renowned for his expertise in financial services compliance, risk management, and audit, Paul is dedicated to promoting financial security for the elderly.

Bert Hofhuis Is a Founder & Entrepreneur Simplifying the Complexities of Later Life Planning. He Navigates the Intricacies of Equity Release, Lifetime Mortgages, Reverse Mortgages, and Wealth Management With Clarity and Expertise.

In his long professional career, Bert has worked with multinational companies and governments, consulting on various financial and logistical projects in Africa, Europe and Asia.

He founded The Enquirer with a team of experienced finance writers and experts to help demystify topics such as equity release, lifetime mortgages, home reversions and retirement interest only mortgages, for people like himself.

TheEnquirer Promise

Expert Verified

Discover the Intricacies of Equity Release & the Critical Role of Professional Guidance. From Understanding Costs to Inheritance Implications, Our Guide Offers Comprehensive Insights to Help You Make Informed Decisions. Dive Into the World of Equity Release Prepared & Confident.

Key Takeaways

Professional equity release advice is important because it ensures you understand the complex features and long-term implications of equity release products, helping you make an informed decision that suits your financial and lifestyle needs.

To find a reputable adviser, look for individuals who are qualified and regulated by the Financial Conduct Authority (FCA), and check if they are members of professional bodies like the Equity Release Council for additional reassurance.

During a session, expect to discuss your financial situation, the types of equity release products, the impact on your estate and benefits, alternative options, and to receive a personalized recommendation.

It can help you avoid common mistakes such as underestimating the impact of compound interest on your loan amount, choosing the wrong type of equity release product, or not considering the effect on your family's inheritance.

It is not always free; many advisers charge a fee for their services, which should be clear and agreed upon before proceeding. Some advisers may offer a free initial consultation, but detailed advice and product recommendations typically come with a cost.

Equity release advice helps navigate the complexities of accessing the value in your property.

The decision to tap into later-life borrowing is quite a significant decision, and having expert guidance can make all the difference.

From understanding the nuances of interest rates to the long-term implications on inheritance, sound advice is crucial.

What You'll Learn in This Article:

This article underscores the importance of seeking informed counsel, highlighting key considerations, and showcasing how expert insights can shape your journey.

Let’s get started.

Who Offers the Lowest Rates in 2025?

Discover the Lowest Rates & Save

Request a FREE call back & discover:

Who offers the LOWEST rates available on the market.

While seeking advice from a qualified advisor is required, it also ensures access to expert knowledge and experience to help you understand the intricacies, explain the potential benefits and risks, and guide you through the entire process.

Comprehensive Assessment

An advisor will thoroughly assess your financial situation, goals, and needs.

They'll consider factors such as your age, your health, your property’s value, any outstanding mortgage, and other factors.

By analysing these variables, they can recommend the most suitable equity release options available to you.

This personalised approach ensures that you can make an informed decision aligned with your individual requirements and objectives.

Protection & Regulation

Equity release is regulated and overseen by various authorities, including the Equity Release Council (ERC)1 and the Financial Conduct Authority (FCA),2 and working with a reputable advisor provides an additional layer of protection.

This decision is a significant financial commitment that can have implications for you and your family, now and in the future.

What Can You Expect From Seeking Equity Release Advice?

You can expect several key elements to be included in the process.

Here's what will typically be included:

Initial Assessment: Your advisor will begin by gathering information about your financial situation, goals, and needs and assess factors such as your age, health, property value, outstanding mortgage, and any existing financial commitments.

Personalised Recommendations: Based on your information and the advisor's assessment, they'll provide personalised recommendations tailored to your specific circumstances.

Costs and Fees: They'll provide a clear breakdown of the costs and fees associated with your selected product options. They'll explain the interest rates, arrangement fees, legal fees, and any other charges you may incur.

Alternatives and Considerations: They'll also explore alternatives such as downsizing, accessing other sources of income, or utilising other financial products.

This comprehensive approach ensures you consider all possibilities, including the risks and benefits, before making a final decision.

How To Choose an Equity Release Advisor

Consider the following steps when you look for an advisor:

Research: Look for advisors with relevant qualifications and experience in equity release. Check their credentials and professional affiliations.

Recommendations: Seek recommendations from friends, family, or trusted financial professionals who have used equity release advisors before.

Reviews and Testimonials: Read online reviews and testimonials to gauge the experiences of previous clients with the advisor.

Interview Multiple Advisors: Speak with multiple advisors to assess their knowledge, communication skills, and willingness to address your concerns.

Regulatory Compliance: Confirm that the advisor is registered with the appropriate regulatory bodies and adheres to industry codes of conduct.

Personal Connection: Choose an advisor with whom you feel comfortable discussing personal financial matters and who understands your unique circumstances.

Professionalism: Look for an advisor who demonstrates professionalism, responsiveness, and a commitment to putting your interests first.

Ongoing Support: Consider whether the advisor offers ongoing support and reviews to ensure your plan remains suitable over time.

Independent Advice: Opt for an independent advisor offering a range of products from different providers, increasing your options.

What’s the Difference Between Financial Advisors & Brokers?

The difference is that financial advisors offer personalised advice and guidance on equity release options based on their expertise.

In contrast, brokers act as intermediaries who connect you with suitable providers and help you secure the best deal.

Both can assist you in navigating the process, but the nature of their roles and how they’re compensated may differ.

Here’s more detail:

Equity Release Financial Advisors

Financial advisors:

Provide personalised advice and guidance on products.

Have in-depth knowledge of the market and regulations.

Typically work independently or as part of financial advisory firms.

Assess your financial situation, discuss your goals and needs, and recommend suitable options based on their expertise.

Provide comprehensive advice, considering your age, health, property value, and outstanding mortgage.

Prioritise understanding your individual circumstances and offering tailored solutions.

Equity Release Brokers

The role of a broker:

Act as intermediaries between you and providers.

Have access to a panel of providers and their products.

Help you navigate the available options and connect you with a suitable provider based on your requirements.

Compare different products, interest rates, and fees offered by various providers to find the most appropriate solution.

Aim to secure the best deal on your behalf, but are typically remunerated through commissions or fees from the providers they work with.

Are Direct Providers or Advisors Better?

An independent advisor is usually better as they’ll review the full regulated market to find the right company for you, but a direct provider is fine if you’re certain about the lender you want to work with.

Here are the key differences.

Direct Providers

Direct providers are financial institutions that offer equity release products directly to consumers.

Choosing a direct provider means working directly with the company offering the product.

Some potential advantages of this include:

Convenience: Dealing directly with the provider can offer a streamlined and simplified process. Fewer intermediaries may be involved, which could result in a faster application and approval process.

Familiarity with the Product: Direct providers have an in-depth understanding of their own products and can provide detailed information about their offerings, including features, benefits, and potential risks.

Cost Savings: In some cases, direct providers may offer lower fees or reduced costs since no intermediary commissions are involved.

Equity Release Advisors

Some potential advantages of working with an advisor include:

Expertise and Guidance: Advisors have extensive knowledge and experience in the market. They can assess your individual circumstances, explain the options available to you, and guide you toward the most appropriate solution.

Access to Multiple Providers: Advisors can access a wide range of products from various providers. This allows them to compare offerings, interest rates, fees, and terms, ensuring you have access to a comprehensive market analysis and a broader selection of options.

Regulatory Protection: Reputable advisors are regulated by industry bodies, providing an additional layer of protection and ensuring that they act in your best interests.

However

It’s important to note that obtaining advice is compulsory when taking out a scheme, as set out by the Equity Release Council.

Thus, when we refer to choosing between a provider or an advisor, it means choosing between an in-house advisor of the provider or an independent advisor.

Which Equity Release Advisors Are Near Me?

You can find advisors near you and in your area by trying the following:

Online Search: Conduct a search using search engines or online directories, specifying your location and relevant keywords such as "equity release advisors" or "equity release specialists."

Recommendations: Seek recommendations from friends, family, or colleagues who may have worked with advisors in your area.

Professional Associations: Check professional associations and regulatory bodies, such as the UK's Financial Conduct Authority (FCA). They often have directories or search functions to help you find registered advisors in your area.

Financial Institutions: Contact your bank or financial institution to inquire if they have advisors or can provide recommendations.

Remember to conduct due diligence when choosing an equity release advisor. Consider their qualifications, experience, reputation, and regulatory compliance.

How Much Does an Equity Release Advisor Cost?

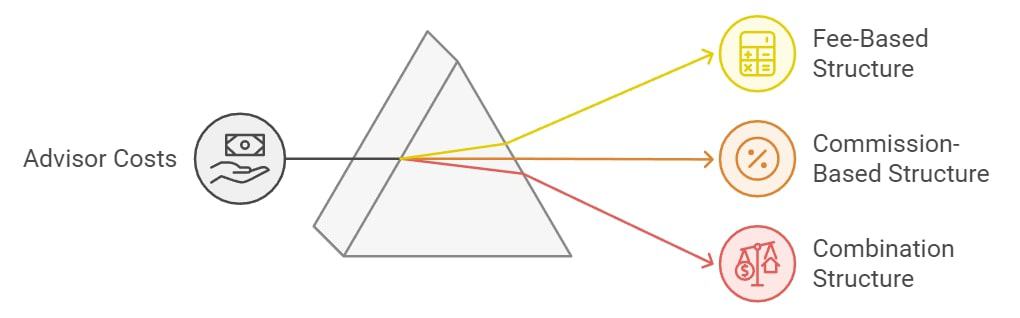

How much an advisor costs can vary depending on several factors, including their fee structure and the complexity of your case.

Here are some common ways that they may charge for their services:

Fee-Based: Some charge a fixed or hourly fee for their services. This fee can vary depending on expertise and the level of support provided throughout the process. The cost is typically agreed upon and disclosed upfront, ensuring transparency.

Commission-Based: In some cases, they may earn a commission from the provider when you proceed with a product they recommended. This commission is typically a percentage of the amount you release or a set fee determined by the provider. It's essential to inquire about potential commissions and their impact on the advisor's recommendations.

Combination: Some advisors may utilise a combination of fees and commissions. They may charge a fee for their advisory services and also receive a commission from the provider if you proceed with a product they recommend.

Therefore, clarifying the fee structure with the advisor before engaging in their services is important.

Transparency regarding costs and fees is crucial in making informed decisions.

Take note!

The cost of working with an advisor can be separate from any fees or charges associated with the scheme, such as arrangement, legal, or valuation fees.

It’s advisable to discuss the cost of working with an advisor directly with them during your initial consultation or interview to ensure you are comfortable with the arrangement and have a clear understanding of the fees involved.

Good Advice Regarding Equity Release

Before proceeding with equity release, take the time to fully understand the implications it may have on your finances, assets, and inheritance.

Consider how it may impact your future financial goals and any potential entitlements or benefits you currently receive. Include your family members or loved ones in the decision-making process and seek their input.

Explore alternatives, such as downsizing or using savings and investments for your needs, as equity release isn’t the only solution for accessing funds in retirement.

Shop around and compare various providers and products to ensure you get the best deal.

And lastly, remember to review your plan regularly. The market evolves and changes, and you may find better interest rates or LTV (loan-to-value) ratios in the future.

Common Questions

Is It Compulsory to Get Equity Release Advice?

Yes, it’s compulsory to get advice.

You won’t be able to get any equity release product without obtaining advice first.

What Information Is Given to Those Requiring Advice?

Those requiring advice are provided with information regarding products' features, benefits, and potential risks.

They receive guidance on the available options, costs, fees, interest rates, and the impact of equity release on their finances and assets.

Advisors also provide personalised recommendations based on the individual's circumstances and goals.

Is There Advice on Retirement Planning Steps?

Yes, advisors can also advise retirement planning steps beyond equity release, including exploring other sources of retirement income, managing savings and investments, and considering options like downsizing or pension plans.

Are There Tips on Choosing the Best Equity Release Advisor?

Yes, here are some tips for choosing the best advisor:

Research their qualifications and experience.

Seek recommendations from trusted sources.

Check for any professional affiliations or regulatory registrations.

Interview multiple advisors to assess their knowledge and communication skills.

Consider their fee structure and how they’re compensated.

Ensure they prioritise understanding your needs and provide personalised recommendations.

Look for a transparent, responsive advisor who acts in your best interests.

What's the Mortgage Advice Bureau?

The Mortgage Advice Bureau (MAB)3 is a leading mortgage intermediary network in the UK.

It comprises a network of mortgage advisors and brokers advising on various mortgage products and services.

MAB works with a panel of providers to offer a wide range of mortgage options to clients.

They aim to help individuals find suitable mortgage solutions based on their needs and circumstances.

In Conclusion

Seeking advice is compulsory, and for good reason.

Advisors provide invaluable guidance and expertise to navigate the complexities of equity release.

With their knowledge and experience, they help you understand the features, benefits, and potential risks of equity release and explore alternative retirement planning steps.

Conduct thorough research, seek recommendations, and interview multiple advisors to find a qualified professional who understands your circumstances, puts your interests first, and can provide the equity release advice you need.

How Does TheEnquirer Ensure Expert-Verified Content?

At TheEnquirer, the integrity and precision of our information is paramount.

Being "expert verified" signifies that our review panel has meticulously assessed each article for precision and comprehensibility. This panel is made up of seasoned professionals in compliance is dedicated to guaranteeing that our content remains impartial and well-informed.

Their rigorous evaluations compel us to maintain a standard of excellence, ensuring that the information we provide is both reliable and of the highest quality.

Financial Guidance Disclaimer for TheEnquirer Readers

Understanding Our Revenue Stream

TheEnquirer operates as an autonomous, ad-supported online platform. Our mission is to furnish you with essential tools and insights for wiser financial choices, granting access to our interactive resources and impartial journalism at no cost.

Please note that while our content is educational, it is not meant as specific financial advice and should not be the only factor in your decision-making. We advise seeking personalized advice from a financial expert to cater to your unique investment needs.

How We Generate Income

Our earnings come from endorsements for products featured on our website. This financial relationship might influence how products are displayed, yet it does not impact the integrity and thoroughness of our information and evaluations. Note that we do not encompass every available financial product or offer.

Commitment to Editorial Integrity

Our reviews are exclusively authored by our editorial staff, reflecting their own views. These insights remain unswayed by our sponsors. At TheEnquirer, we adhere to stringent principles of editorial independence and fairness to ensure unbiased content..

Expert Verified

Expert Verified

How Does TheEnquirer Ensure Expert-Verified Content?

How Does TheEnquirer Ensure Expert-Verified Content?