How Does Equity Release Work? Unraveling the Mysteries

Equity release allows homeowners over 55 to access their property's value as cash, either as a lump sum or in smaller amounts. We find it's a financial decision that needs careful consideration as it involves the home you live in.

Last Updated: 23 Apr 2025

Fact Checked

Our team recently fact checked this article for accuracy. However, things do change, so please do your own research.

Katherine Read is a financial writer known for her work on financial planning and retirement finance, covering equity release, lifetime mortgages, home reversion, retirement planning, SIPPs, pension drawdown, and interest-only mortgages.

Bert Hofhuis Is a Founder & Entrepreneur Simplifying the Complexities of Later Life Planning. He Navigates the Intricacies of Equity Release, Lifetime Mortgages, Reverse Mortgages, and Wealth Management With Clarity and Expertise.

In his long professional career, Bert has worked with multinational companies and governments, consulting on various financial and logistical projects in Africa, Europe and Asia.

He founded The Enquirer with a team of experienced finance writers and experts to help demystify topics such as equity release, lifetime mortgages, home reversions and retirement interest only mortgages, for people like himself.

Paul Derek Sawyer is an esteemed external compliance consultant in equity release, specializing in lifetime mortgages and home reversion plans. With over 20 years of experience, he expertly navigates the complexities of Equity Release Council standards and regulations.

His focus is on ensuring ethical lending practices and safeguarding consumer interests. Renowned for his expertise in financial services compliance, risk management, and audit, Paul is dedicated to promoting financial security for the elderly.

Bert Hofhuis Is a Founder & Entrepreneur Simplifying the Complexities of Later Life Planning. He Navigates the Intricacies of Equity Release, Lifetime Mortgages, Reverse Mortgages, and Wealth Management With Clarity and Expertise.

In his long professional career, Bert has worked with multinational companies and governments, consulting on various financial and logistical projects in Africa, Europe and Asia.

He founded The Enquirer with a team of experienced finance writers and experts to help demystify topics such as equity release, lifetime mortgages, home reversions and retirement interest only mortgages, for people like himself.

TheEnquirer Promise

Expert Verified

Demystifying Home Equity: Understand How It Works, Its Benefits & Risks. But Is It as Simple as It Seems?

Key Takeaways

The steps for releasing equity include seeking advice, choosing a plan, property valuation, application processing, legal checks, and finally receiving the funds.

One of the key benefits is that you can continue living in your home for the rest of your life.

You typically don't make monthly repayments; instead, the loan and interest are repaid when your home is sold, usually upon death or moving into long-term care.

If you move homes, your plan can often be transferred to a new property, subject to your provider's terms and the new property meeting their criteria.

Generally, there are no restrictions on how you use the money, allowing you to spend it on home improvements, travel, gifting to family, or other personal uses.

“How does equity release work?" is a question on the minds of many UK homeowners, especially those looking to maximise their financial assets in later life.

As homes often represent the most significant chunk of personal wealth, understanding the intricacies of equity release can unlock newfound financial freedom.

Could it work for you?

What You'll Learn in This Article:

This in depth guide will help you understand the inns and outs of how these products work, the importance of professional advice, discuss the benefits and potential pitfalls, and and more.

Who Offers the Lowest Rates in 2025?

Discover the Lowest Rates & Save

Request a FREE call back & discover:

Who offers the LOWEST rates available on the market.

In short, equity release works by allowing homeowners to access the value of their property without having to move.

The property serves as collateral against the loan.

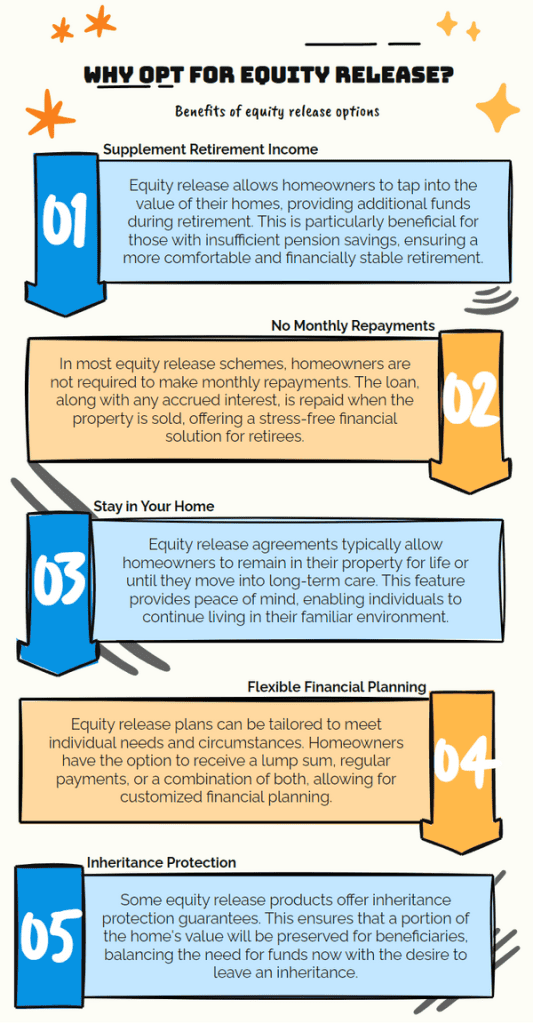

Why Opt for Equity Release?

Equity release offers homeowners a strategic way to tap into the wealth tied up in their property without needing to sell or move.

For many, it presents a solution to diverse financial needs - be it supplementing retirement income, funding home improvements, or even helping grandchildren onto the property ladder.

Types of Equity Release Schemes

The most common form of equity release, a lifetime mortgage, allows you to take a loan against your home's value. You retain ownership and typically don't need to make any repayments until you move out or pass away.

In a home reversion plan, you sell a share of your property to a provider in exchange for a lump sum. You can continue living in the property rent-free until you move or pass on.

Eligibility Criteria

Each provider may have specific prerequisites, but generally, the following are the most common:

Age Requirement: Typically 55+ but varies by provider and plan.

Property Ownership: It's essential that you either own your property entirely or have only a small mortgage remaining. If there's an existing mortgage, the initial funds released must first go towards settling that debt.

Minimum Property Value: The minimum property value can vary depending on the provider and the specific type of scheme. Many providers usually have a minimum property of £70,000.1 However, this figure can vary, and some providers may have a higher threshold.

Property Maintenance: The condition of your home is also taken into account. Homes in good repair and maintained adequately are more likely to meet the criteria for releasing equity.

Health & Lifestyle: Some providers offer enhanced terms if you have specific health conditions or lifestyle habits that might shorten life expectancy, meaning you could potentially release more equity from your home than you initially thought.

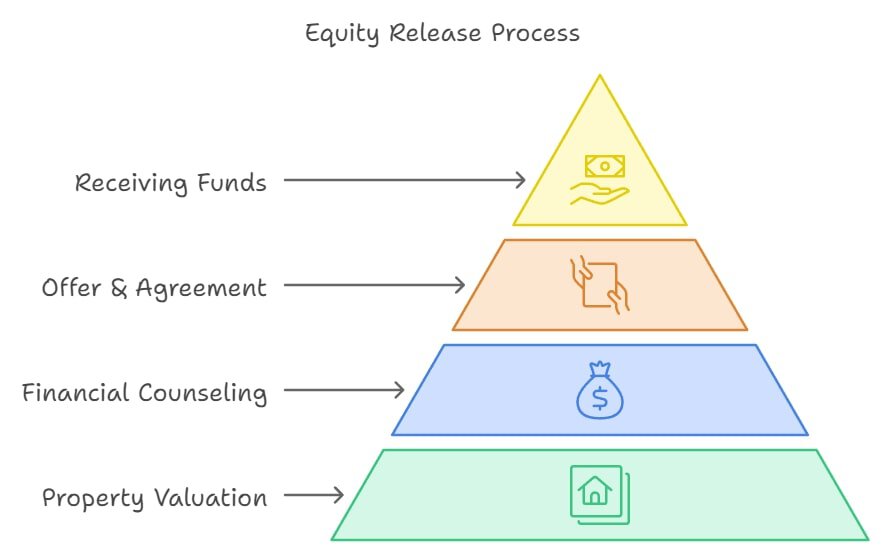

How Does the Process Work?

The equity release process, though meticulous, can be simplified to 4 simple steps

Property Valuation: To determine how much money can be released, a professional valuer will visit and assess various factors of your property, such as its type, condition, size, and geographical location.

Financial Counseling: By consulting a qualified financial advisor or broker, you'll explore the potential advantages, disadvantages, and long-term ramifications. The aim is to equip you with all the information you need to make a decision that aligns with your financial goals.

Offer & Agreement: This document will be comprehensive, outlining the maximum amount you can release, the interest rates, potential charges, and, most importantly, the terms and conditions. It's crucial to scrutinise this offer and seek clarity before proceeding with the agreement.

Receiving Funds: The last step is the release of your funds. Depending on your plan, the agreed amount will be directly deposited into your bank account. Also, some schemes offer a drawdown option, which permits homeowners to access parts of the funds at different times based on their requirements.

When considering equity release as a financial option, seeking professional advice is not just advisable but mandatory.

Here's why professional advice is indispensable:

Understanding the Nuances: Equity release comes with a myriad of intricacies. A professional can help break down the complex terms, conditions, and implications, ensuring that you clearly understand what you're getting into.

Regulatory Mandate: Due to the long-term financial and personal implications associated with these products, it’s mandatory to consult a qualified advisor before proceeding. This requirement ensures that homeowners are adequately protected and are making informed decisions based on expert guidance.

Financial Implications: A specialised financial advisor will assess your current financial status, future projections, and personal needs to determine if releasing your property value is the right fit. They can also guide you on the most suitable type of equity release scheme.

Legal Insights: Beyond the financial aspects, these agreements are legally binding contracts. Legal counsel can clarify your rights, obligations, and potential liabilities within the agreement.

Tailored Recommendations: Every homeowner's situation is unique. Professional advisors can tailor their advice based on your needs, ensuring the plan aligns with your financial goals and personal circumstances.

Benefits of Equity Release

The benefits of releasing equity from your home are myriad, as it provides financial flexibility, requires no monthly payments, and allows you to remain in your home.

Let's explore these benefits in detail:

Financial Flexibility: This newfound financial freedom offers a variety of possibilities, Whether it's to supplement retirement income, make home improvements, or even assist with the educational needs of grandchildren.

No Monthly Repayments: One of the standout features of lifetime mortgages is that there are no monthly repayments. Instead, the loan amount and any accumulated interest are typically repaid when the property is sold, either when you move to long-term care or upon your passing.

Continued Home Ownership: Homeowners retain the ownership and right to reside in their property, ensuring they can continue living in their beloved home, surrounded by familiar comforts and memories, while enjoying the financial benefits.

Potential Pitfalls & Considerations

Potential pitfalls you must be aware of include a reduced inheritance, a potential impact on means-tested benefits, the danger of compound interest, and early repayment charges.

Here’s a breakdown:

Reduced Inheritance: One of the significant considerations is that the amount available to leave as an inheritance might be reduced. As the equity in your home is accessed, the remaining value upon its eventual sale might be diminished.

Impact on Benefits: Proceeds could affect your eligibility for certain means-tested state benefits. Understanding how tapping into your home's equity may alter your benefits status is vital.

Compounding Interest: Particularly in the case of lifetime mortgages, the interest can compound over the years. This means the amount you owe could grow faster than anticipated, especially if no repayments are made.

Early Repayment Fees: Most plans impose charges if you decide to repay the loan earlier than agreed. These fees can be hefty and must be factored in if you're considering an early settlement.

Alternatives to Equity Release

By looking at the alternatives, homeowners can make more informed choices that suit their unique circumstances and long-term goals.

Downsizing: Move to a smaller, cost-effective property and utilise the surplus funds. This option is ideal for homeowners whose current space exceeds their needs, allowing them to monetise unused space while simplifying their lifestyle.

Retirement Interest-Only (RIO) Mortgages: Opt for a mortgage where you only handle the interest payments. The main loan amount is settled when the home is sold, making it a manageable option for retirees with steady income streams.

Unsecured Loans & Government Assistance: Dip into the broader financial realm. Unsecured loans offer quick financial injections without property collateral, while various government schemes provide targeted assistance, from energy grants2 to tax reliefs.3

Remortgaging:Switch your current mortgage deal, either with the same lender or a new one. If your property's value rises rapidly, remortgaging can release some of this increased equity or offer better interest rates.

Mortgage Overpayment: If your mortgage terms allow, overpaying can shrink both the mortgage term and total interest, accelerating the journey to full ownership and subsequent financial freedom.

Home Equity Loan: Obtain a fixed loan using your home's equity as security. Unlike many equity release schemes, this method requires regular monthly repayments, mirroring traditional loan structures.

These bodies set stringent standards and safeguards to protect homeowners' interests.

What Happens if I Decide to Repay My Equity Release Early?

You might face early repayment charges if you decide to repay your plan before the agreed-upon term.

These charges can be a percentage of the amount you're looking to repay and can vary depending on your provider and the specific terms of your agreement.

How Do I Find a Reputable Provider?

To find a reputable provider, opt for one regulated by the FCA and associated with the ERC to ensure adherence to industry standards.

Online reviews on platforms like Trustpilot6 can provide user experiences, while recommendations from acquaintances or financial advisors can offer firsthand insights.

Additionally

Look for providers that showcase transparent practices, diverse product offerings, and strong customer service to ensure a smooth journey.

Can I Still Leave an Inheritance If I Use Equity Release?

Yes. Some plans allow homeowners to ring-fence a portion of the property's value to ensure a specific inheritance for beneficiaries.

However, the total inheritance might be reduced due to the equity released and the accumulated interest.

Is Equity Release Suitable for People Who Have Already Paid off Their Mortgage?

Absolutely. Many homeowners who have cleared their mortgages consider equity release as a means to access funds tied up in their property.

What Are the Tax Implications of Equity Release?

The funds are typically tax-free as they're considered a loan, not income.

However, if you invest this money and earn income from it, that income could be subject to tax.

Furthermore, while equity release itself doesn't change your Inheritance Tax (IHT)7 liability, by decreasing your estate's overall value, it could affect the amount of IHT due in the future

Should I Involve My Family Members in the Equity Release Decision-Making Process?

Yes. Involving your family is often recommended since your decision can impact the inheritance you leave behind.

They might offer a fresh perspective or raise concerns you haven't considered.

Furthermore, open discussions can foster better understanding and avoid potential misunderstandings in the future, ensuring that all parties are aligned with the financial choices being made.

Can I Move House After Releasing Equity?

Typically, yes. Most equity release schemes allow homeowners to relocate, provided the new property meets the provider's criteria.

Any difference in property value might need to be adjusted in the equity release terms.

What Happens to the Equity Release Loan When I Pass Away?

Upon passing or moving into long-term care, your property is usually sold, and the proceeds are used to repay the equity release loan and any accrued interest.

Any remaining funds are then passed to your beneficiaries.

In Conclusion

While it promises various benefits, like financial flexibility and no mandatory monthly repayments, it's vital to approach equity release with due diligence - Making sure to understand each stage of the process, from property valuation to fund disbursement, is crucial.

Furthermore, acknowledging potential drawbacks and consulting with family members ensures an all-rounded, informed decision.

As with all financial ventures, seeking professional advice and understanding the full spectrum of available options guarantees that homeowners harness the true potential of their property wealth and fully understand ‘how does equity release work’.

Editorial Note: This content has been independently collected by the SovereignBoss team and is offered on a non-advised basis. SovereignBoss may earn a commission on sales made from partner links on this page, but that doesn’t affect our editors’ opinions or evaluations. Learn more about our editorial guidelines.

How Does TheEnquirer Ensure Expert-Verified Content?

At TheEnquirer, the integrity and precision of our information is paramount.

Being "expert verified" signifies that our review panel has meticulously assessed each article for precision and comprehensibility. This panel is made up of seasoned professionals in compliance is dedicated to guaranteeing that our content remains impartial and well-informed.

Their rigorous evaluations compel us to maintain a standard of excellence, ensuring that the information we provide is both reliable and of the highest quality.

Financial Guidance Disclaimer for TheEnquirer Readers

Understanding Our Revenue Stream

TheEnquirer operates as an autonomous, ad-supported online platform. Our mission is to furnish you with essential tools and insights for wiser financial choices, granting access to our interactive resources and impartial journalism at no cost.

Please note that while our content is educational, it is not meant as specific financial advice and should not be the only factor in your decision-making. We advise seeking personalized advice from a financial expert to cater to your unique investment needs.

How We Generate Income

Our earnings come from endorsements for products featured on our website. This financial relationship might influence how products are displayed, yet it does not impact the integrity and thoroughness of our information and evaluations. Note that we do not encompass every available financial product or offer.

Commitment to Editorial Integrity

Our reviews are exclusively authored by our editorial staff, reflecting their own views. These insights remain unswayed by our sponsors. At TheEnquirer, we adhere to stringent principles of editorial independence and fairness to ensure unbiased content..

Expert Verified

Expert Verified

How Does TheEnquirer Ensure Expert-Verified Content?

How Does TheEnquirer Ensure Expert-Verified Content?