Equity Release: Unlocking Financial Freedom in Retirement

Equity release allows homeowners over 55 to access their property's value as cash, either as a lump sum or in smaller amounts. We find it's a financial decision that needs careful consideration as it involves the home you live in.

Last Updated: 22 Apr 2025

Fact Checked

Our team recently fact checked this article for accuracy. However, things do change, so please do your own research.

Katherine Read is a financial writer known for her work on financial planning and retirement finance, covering equity release, lifetime mortgages, home reversion, retirement planning, SIPPs, pension drawdown, and interest-only mortgages.

Bert Hofhuis Is a Founder & Entrepreneur Simplifying the Complexities of Later Life Planning. He Navigates the Intricacies of Equity Release, Lifetime Mortgages, Reverse Mortgages, and Wealth Management With Clarity and Expertise.

In his long professional career, Bert has worked with multinational companies and governments, consulting on various financial and logistical projects in Africa, Europe and Asia.

He founded The Enquirer with a team of experienced finance writers and experts to help demystify topics such as equity release, lifetime mortgages, home reversions and retirement interest only mortgages, for people like himself.

Paul Derek Sawyer is an esteemed external compliance consultant in equity release, specializing in lifetime mortgages and home reversion plans. With over 20 years of experience, he expertly navigates the complexities of Equity Release Council standards and regulations.

His focus is on ensuring ethical lending practices and safeguarding consumer interests. Renowned for his expertise in financial services compliance, risk management, and audit, Paul is dedicated to promoting financial security for the elderly.

Bert Hofhuis Is a Founder & Entrepreneur Simplifying the Complexities of Later Life Planning. He Navigates the Intricacies of Equity Release, Lifetime Mortgages, Reverse Mortgages, and Wealth Management With Clarity and Expertise.

In his long professional career, Bert has worked with multinational companies and governments, consulting on various financial and logistical projects in Africa, Europe and Asia.

He founded The Enquirer with a team of experienced finance writers and experts to help demystify topics such as equity release, lifetime mortgages, home reversions and retirement interest only mortgages, for people like himself.

TheEnquirer Promise

Expert Verified

Unlocking Home Equity: Discover the Benefits, Myths & Hidden Potentials in Our Comprehensive Guide. But What's the Catch?

Key Takeaways

Equity release is a financial option allowing homeowners over 55 to unlock the value of their property as either a lump sum or regular payments, while retaining ownership.

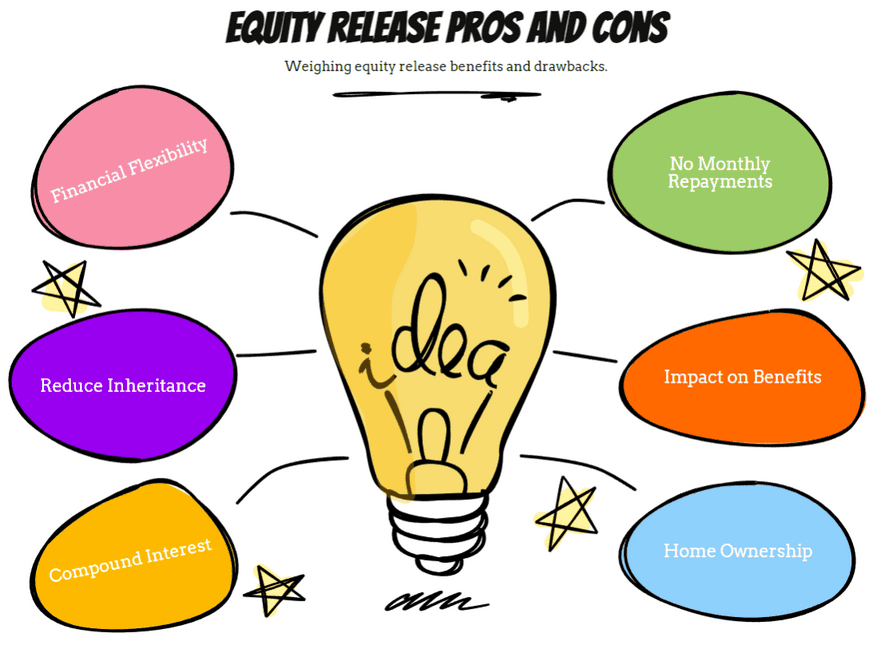

By accessing the equity tied up in your home, it provides a supplement to your retirement income, enhancing your financial flexibility.

The benefits include accessing cash without moving out, but it's essential to consider downsides such as reduced inheritance for heirs and the accumulation of interest.

Alternatives include downsizing, borrowing against other assets, or seeking family assistance, each with its own implications for your financial and living situation.

Selecting the best scheme requires comparing interest rates, flexibility, and terms across providers, alongside consulting with a financial advisor to align with your retirement goals.

Do You Want to Learn More About Releasing Equity from Your Home? Find Out How to Get EXPERT Equity Release Advice & Enjoy a Simple Overview of Equity Release.

According to statistics, UK homeowners released over £4,8 billion2 in property wealth in 2021 and, during the first half of 2022, £3,13 billion3. With everyone asking, what's equity release, we've decided to break it down in detail for you.

If you're retired or starting to plan your later-life finances, now's the time to find out whether equity release could be a suitable option for you.

At TheEnquirer, we've spent countless hours engrossed in the latest developments in the later-life finance sector, so we’re in an ideal position to help you learn more about equity release.

Depending on your individual needs, an equity release mortgage could be the solution you’ve been looking for.

Continue reading to find out more.

What You'll Learn in This Article:

Who Offers the Lowest Rates in 2025?

Discover the Lowest Rates & Save

Request a FREE call back & discover:

Who offers the LOWEST rates available on the market.

Equity release in the UK is an umbrella term for financial products that let UK homeowners aged 55 or over release tax-free funds from their homes.

A lender will calculate the amount you could release based on the age of the youngest applicant (if you're making a joint application) and the value of your property.

You may want to do so if interest rates have dropped or if you come across a better deal.

While interest rates are increasing, plans are vastly more flexible than they were a few years ago.

If you wish to consider switching equity release plans or providers, we suggest you contact a specialist financial advisor or broker to assist you through the process.

Your advisor will determine whether equity release suits your individual needs and will assist you in finding the right plan for you. They’ll also help you submit your application and will be able to assist you until your application is complete.

It usually takes about 12 weeks from the date of application for the process to be completed4.

What Are the Main Equity Release Uses?

The main equity release uses are to achieve your financial goals, from covering your basic living expenses to allowing you to indulge in a dream holiday.

Whatever you'd like to use the money for, you must consult a qualified financial advisor who can find the product that best suits your circumstances.

Are There Restrictions on How I Can Use the Money Released From My Property?

Yes, there are restrictions on how you can use the money released from your property.

Illegal activities are a clear no, but there's not many legal restrictions on how the money is used.

Lenders won't give you the money to use for gambling or risky investment opportunities.

The exact cost breakdown will depend on the vendors you select, but your financial advisor will provide a precise quote before you finally accept the offer.

These costs cover the following services:

Advice fees

Arrangement fees

A surveyor's bill

Legal fees

Some of these fees may be waived by your lender or offered free as a part of your equity release package.

How Can I Reduce Equity Release Costs?

You can reduce equity release costs by considering the following steps:

Repaying the interest monthly to stop it from compounding.

Repaying a portion of the loan annually to reduce the overall loan amount.

Finding a lender that offers free advice or waves the valuation fee.

Is Equity Release Expensive?

Equity release is expensive as interest rates can be higher than 8%6.

At the end of 2020 and during 2021, interest rates plummeted to an all-time low but have since risen7.

When Is Equity Release Repaid?

Equity release is repaid from your property sale's income when you pass away or move to long-term care.

However, you can repay some of the loan and the monthly interest.

These products allow you to sell all or part of your home below market value to a home reversion provider, with a lifetime tenancy included in the deal.

What's the Most Popular Type of Equity Release?

The most popular type of equity release is a lifetime mortgage.

According to the Equity Release Council's Q3 2022 statistics, 52% of customers chose lump sum lifetime mortgages and 48% drawdown lifetime mortgages, with no mention of a home reversion scheme8.

Equity Release Locations: Is It Available Where I Live?

Regarding equity release locations, it's available if you live in most parts of the UK and surrounding islands. Where you live may impact which lenders are available to you.

If you live on one of the Scottish Isles, the Isle of Man, or in Northern Ireland, your options may be more limited.

Equity release is a big financial decision that can't be taken without the guidance of a financial advisor.

Make sure you choose a qualified advisor approved by the Equity Release Council.

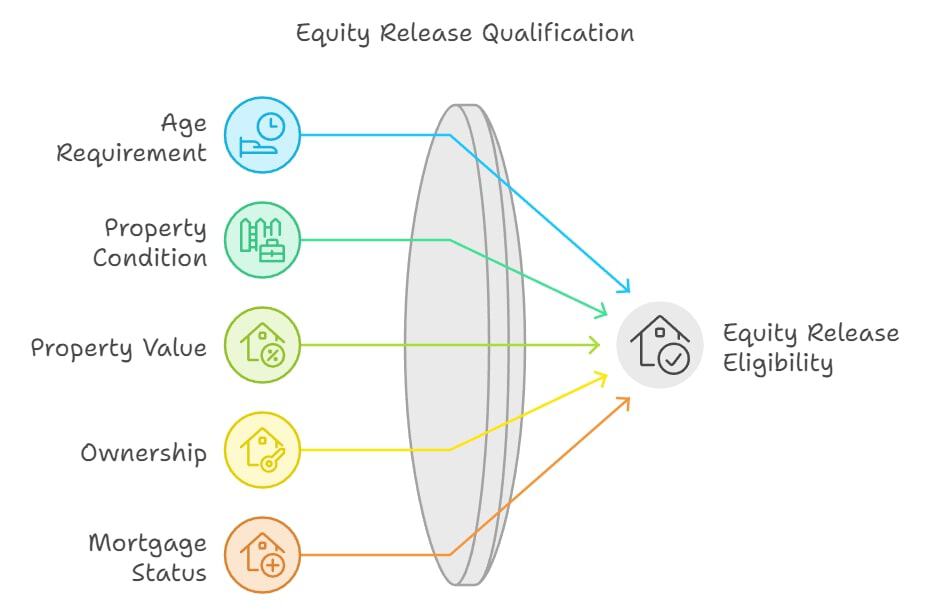

How Much Equity Can I Release From My Property?

How much equity you'll be able to release from your property will depend on your age and the value of your property, and in the case of an enhanced lifetime mortgage, your health.

You'll usually be able to access between 20% and 60% of the market value of your property9.

Equity release vs downsizing is an age-old debate. While some retirees prefer a smaller space and less maintenance, others treasure their homes and have little desire to pack up and clear out.

It's best to discuss these options with your family and financial advisor.

Equity Release vs Retirement Interest-Only Mortgages

RIOs are newer products but have yet to catch on in popularity compared to an equity release mortgage.

While there's no monthly repayment obligations with an equity release loan, you're required to pay an RIO’s monthly interest, and you can risk losing your property if you fail to do so.

On the other hand, a lifetime mortgage guarantees the right to remain in your home until you pass away or move to a care home.

Is Equity Release a Good Idea?

Equity release is a good idea if you've considered all the alternatives and sought approval from a regulated financial advisor or broker.

Here's some questions to consider when weighing up if equity release is a good idea:

Can I Lose My House After I've Released Equity?

No, you can’t lose your home if you’ve opted for an equity release deal, provided you abide by the terms of your contract.

What's the Catch With Equity Release?

The catch with equity release is that no repayments don't mean nothing is owed. The cash you unlock will need to be repaid when you pass away or move into long-term care.

With a lifetime mortgage, you’ll owe the capital borrowed and compound interest accrued on the loan.

You don't have to unlock all your property value in one go. Instead, you can opt for a drawdown lifetime mortgage. These products allow you to withdraw an initial lump sum before placing the balance in a reserve cash facility that can be accessed incrementally whenever you wish. There's a minimum amount usually prescribed by lenders.

You'll still have full property ownership if you opt for a lifetime mortgage equity release.

You can still move home if you opt for equity release. You'll need to find a property approved by your lender, or you might face early repayment charges. Either way, equity release doesn't necessarily tie you to your property for life.

You can opt for downsizing protection to avoid penalties if you pay off your loan to move to a smaller property later.

Equity Release Horror Stories: Are these Relevant in 2025?

The biggest horror stories include debt that doubles or owing more than what the property is worth.

Fortunately, these myths can be debunked:

While equity release debt can double, this is avoidable by repaying the interest and monthly increments whenever you can.

Thanks to a ruling by the Equity Release Council, the 'no negative equity guarantee' means that if you opt for equity release, your family won’t be left with crippling debt. Instead, your lender will write off all additional debt.

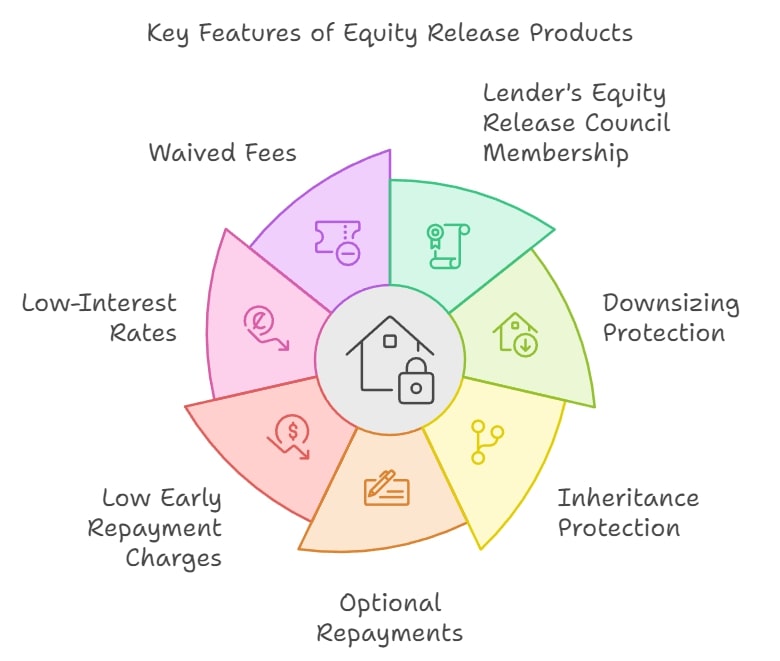

What Are the Equity Release Product Features to Look Out For?

The equity release product features to look out for are those that will best serve you financially.

Here's some important features:

The lender holds Equity Release Council membership.

Downsizing protection

Inheritance protection

Allows optional repayments on your loan and interest.

Low early repayment charges

Relatively low-interest rates

Waives certain fees without impacting the overall equity release costs.

However, it's important to remember that your unique circumstances and financial goals will determine the best equity release scheme for you.

Which Equity Release Companies Should I Avoid?

You should avoid equity release companies that aren't members of the Equity Release Council or regulated by the Financial Conduct Authority.

You'll spot these companies if they don’t offer the following:

No negative equity guarantee – Designed to ensure your family isn't left with unpayable debt after you've passed away or entered long-term care.

Capped variable or fixed interest rates – Uncapped interest rates could mean your rates skyrocket beyond reason.

Voluntary loan or interest repayments – You must have the opportunity to avoid mounting compound interest.

Thorough reviews of your circumstances alongside professional financial advice – An immediate loan, online or in-person, without reviewing your circumstances is a big no.

While the industry was once riddled with corruption, modern rules have put an end to this.

Here's more details.

Who Regulates the Equity Release Industry?

The Equity Release Council and Financial Conduct Authority regulate the equity release industry.

What's the Equity Release Council?

The Equity Release Council was implemented to oversee the equity release sector and ensures the promotion of high standards of conduct and practice throughout the industry.

Whether it's initial equity release advice or any part of the journey, safeguarding the consumer is the Council's primary mission.

Since equity release is a financial product, it falls under the FCA's portfolio.

Is There a List of Regulated Equity Release Providers?

There is a list of regulated equity release providers on the Equity Release Council's website here.

Will I Pay Equity Release Tax?

You won't pay equity release tax when selecting one of these products. It's exempt from income tax as it’s not a salary, even if you use it to supplement yours.

However, the way you use your funds could incur a tax liability for you or the recipient of the funds.

Additionally, if you gift the money and you die within 7 years of gifting it, the recipient pays taxes on that.

Is Equity Release Safe?

Equity release is safe if you seek professional advice and opt for a lender that’s an active Equity Release Council member and regulated by the Financial Conduct Authority.

What Safety Features Should I Look Out For?

You should look out for the following safety features when opting for equity release:

An Equity Release Council membership

The 'no negative equity guarantee'

Inheritance protection

Downsizing protection

The right to move home

Plans suggested by a qualified financial advisor

The right to remain in your home until you pass away or need to move to long-term care.

Will Equity Release Impact My Family's Inheritance?

Equity release will impact your family's inheritance.

For most retirees in the UK, your home is your largest asset12, so by using your property's value during your lifetime, you're leaving less to your beneficiaries and heirs when you die.

Can I Lose My House After an Equity Release?

You can't lose your home with equity release if you stick to the terms and conditions of your plan.

The Equity Release Council has set out to ensure that homeowners can retain property residency, even after equity release.

4 Things to Consider with Equity Release

There are 4 things to consider with equity release, including the impact on inheritance, claiming of benefits, negative equity, and the costs involved.

Here's more information.

Impact on Inheritance

Fortunately, you can opt for a plan with inheritance protection to set aside a portion of your estate for a guaranteed inheritance that your equity release provider or plan can’t touch.

Claiming Benefits

Claiming benefits can be tricky with equity release, so you must discuss this with your financial advisor.

Equity release may impact your means-tested benefits because you may no longer qualify.

With a regulated lender, your family is guaranteed to have the means to settle their debt by selling your property.

Costs Involved

There are costs involved with equity release, like all financial products.

The highest cost is interest, which will be left to compound if not repaid.

What's the Evolution of Equity Release & It's History?

The evolution of equity release and it's history includes the first plans being arranged in the late 1970s, with the market remaining unpopular for years to come.

Equity release began to rise in popularity in 2010 and has since strengthened. The total released quadrupled in the first 8 years of its rise to popularity.

A lack of regulation or safety practices in the 80s meant that the industry was riddled with fraud, triggering the formation of the Equity Release Council13.

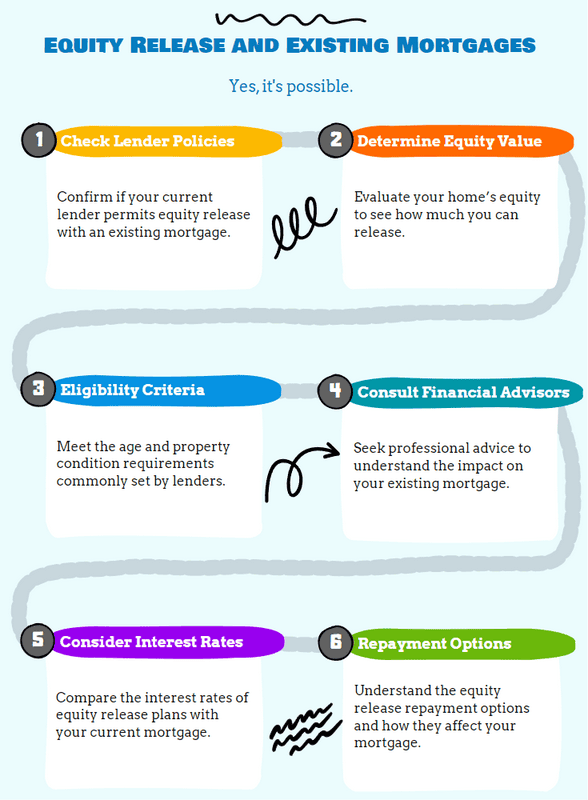

What Are Common Equity Release Myths?

Common equity release myths include that you can't get equity release with an existing mortgage.

This isn't true

On the contrary, you can use equity release to pay off your mortgage, or if there's a small existing balance, you will need to settle that before unlocking a remaining balance.

Of course, if your mortgage is larger than the maximum equity available to unlock, you won’t qualify.

Equity release is more popular than ever, with a record 13,452 new plans signed between July and September 202214.

These statistics are worth your consideration when shopping for an equity release plan.

Should I Consider Equity Release in 2025?

You should consider equity release in 2025 if you've reviewed all your alternatives and received a green light from a professional financial advisor or broker specialising in these products.

With rising interest rates, you must ensure it’s the best option for you and your family.

Common Questions

What Does Equity Release on a Property Mean?

Equity release from your property means unlocking all or a portion of your property value while still making use of it as your primary residence (a 2nd home in some cases).

Should I Be Concerned About Rising Equity Release Interest Rates?

You should be concerned with rising equity release interest rates if you’re a potential new customer since higher rates means more interest to repay on your loan.

Your best bet is to mention rising interest rates to your financial advisor or broker, who can provide advice on the matter.

Is Equity Release More Expensive Than a Regular Mortgage?

Yes, equity release is more expensive than a regular mortgage, primarily when referring to interest rates.

Equity release interest rates start at 6.87% and rise to 9% AER*.

Mortgage rates have also risen but are currently peaking at 6.65%15.

Can I Remortgage My Existing Equity Release Loan?

You can remortgage your existing equity release loan if you’re unhappy with your plan.

Your best bet is to chat with a financial advisor.

Some factors to consider concerning remortgaging your existing plan:

Rising interest rates – you likely paid less if you used equity release in the last 2 years.

The guaranteed option of partial repayments was implemented for all new plans since 31 March 2022.

Newer flexible plans and deals.

Whether you qualify for the latest plan developments.

The amount outstanding on your equity release plan and any interest accrued.

Is equity release right for me? Is a question that doesn’t have a ‘one size fits all’ answer.

This can only be known after exploring your options and chatting with a financial advisor or broker.

Will Equity Release Affect My Benefits?

Equity release could affect your state and means-tested benefits now or in the future, as will be highlighted by your financial advisor or broker.

Will I Get the True Market Value of My Property if I Opt for Equity Release?

You won't get actual market value on your property if you opt for equity release. Instead, you can only access a portion of your estate as some or all of the rest of the estate value will be used to cover interest costs.

Consider selling if you'd prefer to benefit from your property’s total value.

Can I Unlock Equity More Than Once on the Same Property?

You can unlock equity more than once on a property, likely for one of the following reasons:

You've only unlocked a small portion, and there’s leftover income.

You opted for a drawdown lifetime mortgage.

You've repaid your equity release loan.

Can You Pay Back an Equity Release Loan Early?

You can pay back your equity release loan early, but you may incur early repayment charges.

These will usually fall between 1% and 8% of your total loan amount16.

Is Getting an Equity Release Mortgage Easy?

If you qualify, getting an equity release mortgage is a relatively easy process. Thanks to your financial advisor or broker, you’ll have guidance throughout the experience.

In Conclusion

Equity release is a unique financial product designed especially for homeowners over 55. If you fall into this category and want to free up some cash, you should seek financial advice.

Now that you know, 'what's equity release', you're ready to have an informed conversation with an advisor, whether it's your first appointment or you're looking to switch plans.

How Does TheEnquirer Ensure Expert-Verified Content?

At TheEnquirer, the integrity and precision of our information is paramount.

Being "expert verified" signifies that our review panel has meticulously assessed each article for precision and comprehensibility. This panel is made up of seasoned professionals in compliance is dedicated to guaranteeing that our content remains impartial and well-informed.

Their rigorous evaluations compel us to maintain a standard of excellence, ensuring that the information we provide is both reliable and of the highest quality.

Financial Guidance Disclaimer for TheEnquirer Readers

Understanding Our Revenue Stream

TheEnquirer operates as an autonomous, ad-supported online platform. Our mission is to furnish you with essential tools and insights for wiser financial choices, granting access to our interactive resources and impartial journalism at no cost.

Please note that while our content is educational, it is not meant as specific financial advice and should not be the only factor in your decision-making. We advise seeking personalized advice from a financial expert to cater to your unique investment needs.

How We Generate Income

Our earnings come from endorsements for products featured on our website. This financial relationship might influence how products are displayed, yet it does not impact the integrity and thoroughness of our information and evaluations. Note that we do not encompass every available financial product or offer.

Commitment to Editorial Integrity

Our reviews are exclusively authored by our editorial staff, reflecting their own views. These insights remain unswayed by our sponsors. At TheEnquirer, we adhere to stringent principles of editorial independence and fairness to ensure unbiased content..

Expert Verified

Expert Verified

How Does TheEnquirer Ensure Expert-Verified Content?

How Does TheEnquirer Ensure Expert-Verified Content?