Switching equity release plans can offer lower interest rates or better terms. We recommend exploring the market for remortgage options and seeking advice to understand the potential benefits and costs.

Last Updated: 02 Mar 2025

Fact Checked

Our team recently fact checked this article for accuracy. However, things do change, so please do your own research.

Katherine Read is a financial writer known for her work on financial planning and retirement finance, covering equity release, lifetime mortgages, home reversion, retirement planning, SIPPs, pension drawdown, and interest-only mortgages.

Bert Hofhuis Is a Founder & Entrepreneur Simplifying the Complexities of Later Life Planning. He Navigates the Intricacies of Equity Release, Lifetime Mortgages, Reverse Mortgages, and Wealth Management With Clarity and Expertise.

In his long professional career, Bert has worked with multinational companies and governments, consulting on various financial and logistical projects in Africa, Europe and Asia.

He founded The Enquirer with a team of experienced finance writers and experts to help demystify topics such as equity release, lifetime mortgages, home reversions and retirement interest only mortgages, for people like himself.

Paul Derek Sawyer is an esteemed external compliance consultant in equity release, specializing in lifetime mortgages and home reversion plans. With over 20 years of experience, he expertly navigates the complexities of Equity Release Council standards and regulations.

His focus is on ensuring ethical lending practices and safeguarding consumer interests. Renowned for his expertise in financial services compliance, risk management, and audit, Paul is dedicated to promoting financial security for the elderly.

Bert Hofhuis Is a Founder & Entrepreneur Simplifying the Complexities of Later Life Planning. He Navigates the Intricacies of Equity Release, Lifetime Mortgages, Reverse Mortgages, and Wealth Management With Clarity and Expertise.

In his long professional career, Bert has worked with multinational companies and governments, consulting on various financial and logistical projects in Africa, Europe and Asia.

He founded The Enquirer with a team of experienced finance writers and experts to help demystify topics such as equity release, lifetime mortgages, home reversions and retirement interest only mortgages, for people like himself.

TheEnquirer Promise

Expert Verified

Considering Switching Your Equity Release Plan? Dive Into the UK’s Evolving Financial Landscape & Uncover the Key Reasons, Benefits, & Steps to Ensure a Seamless Transition. Make an Informed Choice for a Brighter Financial Tomorrow.

Key Takeaways

You can switch your plan to another provider, a process known as equity release remortgaging, which may offer you more favorable terms or features than your current plan.

The costs involved can include early repayment charges on your current plan, application fees, valuation fees, and legal fees for the new plan, which can vary widely between providers.

Before switching, consider factors such as the size of any early repayment charges, the benefits of the new plan versus your current one, changes in interest rates, and your long-term financial needs.

It can affect your loan amount, potentially allowing you to access more equity due to changes in property value, your age, or improved terms with a new provider, though this can also mean increased costs over time due to compounding interest.

Benefits can include lower interest rates, more flexible withdrawal options, or more favorable loan terms, which can reduce the long-term cost of the loan or better suit your current financial situation.

Switching equity release plans is a decision that more UK homeowners are considering as the financial landscape evolves.

While equity release offers a valuable means to access the wealth tied up in one's property, ensuring the plan aligns with current market conditions and personal financial goals is paramount.

As homeowners seek better interest rates, enhanced features, or a response to changing life circumstances, understanding the why, when, and how of making a switch becomes crucial.

What You'll Learn in This Article:

Dive in as we unravel the intricacies of this process, ensuring you're equipped with the knowledge to make an informed choice.

Who Offers the Lowest Rates in 2025?

Discover the Lowest Rates & Save

Request a FREE call back & discover:

Who offers the LOWEST rates available on the market.

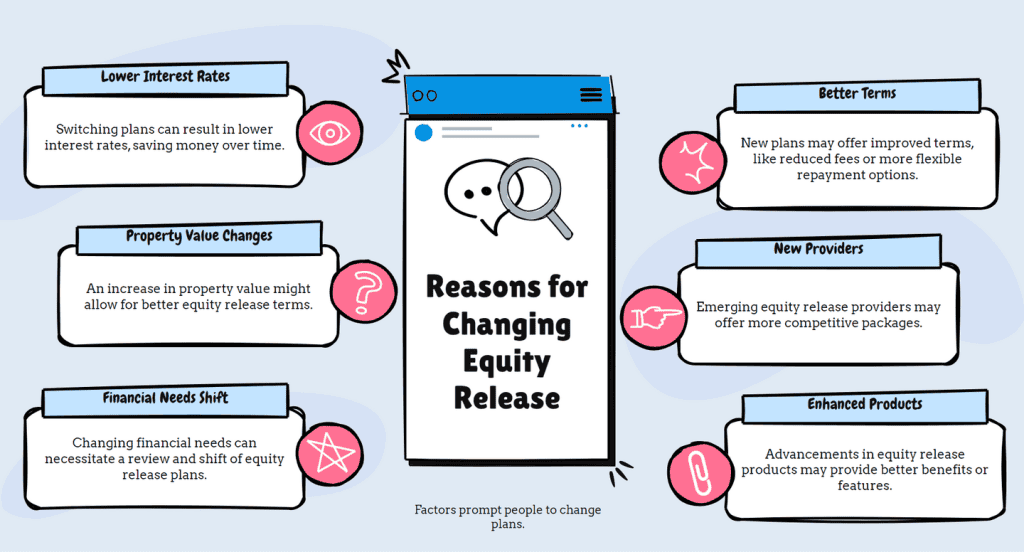

Switching plans might be a good idea in the constantly evolving financial marketplace, where equity release products aren’t exempt from changes.

New and competitive products frequently enter the market, interest rates fluctuate, and your personal circumstances might shift.

Here are a few reasons why one might consider switching:

More Competitive Interest Rates: Like traditional mortgages, newer equity release plans may offer more attractive interest rates than your current plan, depending on when you opted for your original product.

Changing Financial Needs: Over time, you might require more funds than initially anticipated or want to reduce the money drawn down.

Improved Plan Features: New plans may offer better features, such as flexible repayment options, inheritance protection, or partial repayments without penalties.

Understanding the Terms: Porting, Refinancing, and Switching

The terminology around changing equity release plans can be confusing, but knowing the difference between porting, refinancing, and switching is essential.

It's crucial to understand these terms to make informed decisions:

Porting - This refers to transferring your existing equity release plan to a new property. If you're looking to move homes and want to take your current agreement with you, then porting could be the option to consider. Not all plans offer this flexibility, so checking with your provider is crucial.

Refinancing - This involves replacing your existing equity release plan with a new one, often to benefit from better terms or features. This is similar to remortgaging a traditional mortgage. Before refinancing, consider any potential penalties, costs, or fees associated with ending your current plan early.

Switching - This broader term can encompass both porting and refinancing. It generally refers to changing from your existing scheme to a new scheme, irrespective of the reason. Switching might involve moving to a different provider or sticking with your current provider on a different plan.

Key Considerations Before Making the Switch

Before switching equity release plans, here are some essential key considerations:

Potential Early Repayment Charges - Switching before your plan's term ends can often incur early repayment charges. These charges can sometimes be substantial, so weighing these against the potential benefits of switching to a new plan is vital.

Valuation Fees and Other Associated Costs - Switching may come with other costs, such as new valuation1 fees for your property. There may also be application fees or adviser charges associated with the new plan. Ensure you factor in all these costs when determining if it's financially beneficial to make the switch.

Impact on Your Beneficiaries and Estate - Equity release reduces your estate's value, impacting the inheritance you'll leave behind. Switching plans, especially if you're releasing more equity, can further reduce what's left for your beneficiaries.

And remember

Beyond the initial costs, there may be hidden fees and long-term financial implications.

While the newer plans may seem advantageous on the surface, it's essential to factor in all possible drawbacks.

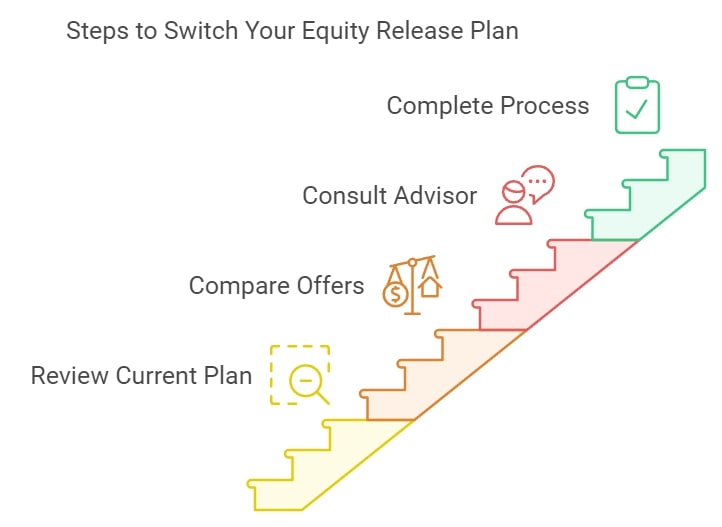

Steps to Switch Your Equity Release Plan

Here's a step-by-step guide to help you through the process of switching your equity release plan.

Review Your Current Plan's Terms and Conditions

Before deciding if switching is the right choice for you, it's imperative to understand your current plan inside out.

Penalties and Charges: Look for any early repayment charges or exit fees that might apply if you switch before the term ends.

Features and Benefits: Ensure you're not losing out on any valuable features your current plan offers, which may not be present in a new one.

Compare New Equity Release Offers

Once familiar with your current plan, start exploring the market for newer options.

Interest Rates: Look for plans with competitive rates. Even a slight difference can mean significant savings over time.

Plan Features: Some newer plans may offer more flexibility, such as voluntary repayments, inheritance protection, or drawdown facilities.

Consult a Financial Advisor or Equity Release Specialist

Personalised Recommendations: An advisor can provide tailored suggestions based on your needs, financial situation, and property value.

Market Insight: Equity release specialists have a pulse on current market trends and can advise on the best times to switch or potential future developments.

Completing the Switching Process

If you've decided that switching is the right move, the final step is to complete the transition.

Application: Begin by filling out an application for the new equity release plan.

Property Valuation: The new provider typically requires an updated property valuation to determine how much equity you can release.

Legalities: A solicitor2 will need to oversee the legal process of closing your old plan and opening the new one. This involves settling any remaining debt with your current provider using the funds from the new plan and releasing any additional funds to you.

Common Mistakes to Avoid When Switching Equity Release Plans

Understanding common mistakes made during the switching process can sidestep them and ensure a smoother transition to a new equity release plan that better serves your needs.

Don’t forget to receive the right financial advice, review the fine print of your new plan, and review future market conditions.

Here’s a breakdown.

Not Seeking Independent Advice

While making decisions without consulting an expert might seem cost-effective, this can often lead to unintended consequences.

Biassed Opinions: Relying solely on advice from the new provider may not give you a comprehensive view. They may be more interested in selling their product rather than ensuring it's the best fit for you.

Complexity of Products: Equity release products can be intricate, with various features and clauses. An independent adviser can clarify and help you understand how different plans align with your goals.

Misjudging Future Market Conditions

The financial market is ever-evolving, and while no one can predict its exact trajectory, some foresight can avoid potential pitfalls.

Fixed vs. Variable Rates: While fixed rates can offer stability, they may not always be the best choice if market conditions suggest that interest rates will fall in the future. Presently, lenders offer plans with fixed rates, but some have offered variable, capped rates.

Potential Market Developments: The equity release market continually innovates, regularly introducing new products and features.3 Switching too hastily might mean missing out on an even better product just around the corner.

Overlooking the Fine Print and Hidden Costs

The allure of a new equity release plan, especially one with a seemingly lower interest rate, can sometimes overshadow the more minor details.

Hidden Fees: It's crucial to account for all potential costs, such as application fees, valuation charges, and administrative costs. These can quickly add up and reduce the financial benefits of switching.

Terms and Conditions: Always read the fine print. Some plans may come with clauses that aren’t immediately apparent but could be restrictive or costly in the long run.

Common Questions

Can I Switch My Equity Release Plan if I've Moved to a Different Home?

Yes, you can, but it depends on the terms of your existing plan.

Some equity release schemes offer the option of "porting" your plan to a new property.

How Do Changes in the Bank of England's Base Rate Affect Equity Release Interest Rates?

Changes in the Bank of England's base rate4 can influence the interest rates set by equity release providers, especially if your plan has a variable interest rate.

However, many equity release plans come with fixed rates, which wouldn't be affected by changes in the base rate during the fixed term.

Always check the specific terms of your plan.

What Are the Tax Implications of Switching Plans?

Switching an equity release plan doesn't directly create a tax liability.

Still, the money you release and how you use it can have tax implications.

For instance, investing the released funds and earning interest could be subject to income tax.

Always consult with a tax adviser to understand potential implications for your circumstances.

In Conclusion

Navigating the intricacies of your financial future can be challenging, but making informed choices can ensure long-term benefits.

Switching your equity release scheme may seem daunting, but careful consideration and expert guidance can open up new possibilities and better financial terms.

Whether to leverage better interest rates, capitalise on improved market conditions, or access more from your property's value, remember that the goal is to enhance your financial well-being.

Ultimately, switching equity release plans might be the pivotal step toward a more secure financial future.

How Does TheEnquirer Ensure Expert-Verified Content?

At TheEnquirer, the integrity and precision of our information is paramount.

Being "expert verified" signifies that our review panel has meticulously assessed each article for precision and comprehensibility. This panel is made up of seasoned professionals in compliance is dedicated to guaranteeing that our content remains impartial and well-informed.

Their rigorous evaluations compel us to maintain a standard of excellence, ensuring that the information we provide is both reliable and of the highest quality.

Financial Guidance Disclaimer for TheEnquirer Readers

Understanding Our Revenue Stream

TheEnquirer operates as an autonomous, ad-supported online platform. Our mission is to furnish you with essential tools and insights for wiser financial choices, granting access to our interactive resources and impartial journalism at no cost.

Please note that while our content is educational, it is not meant as specific financial advice and should not be the only factor in your decision-making. We advise seeking personalized advice from a financial expert to cater to your unique investment needs.

How We Generate Income

Our earnings come from endorsements for products featured on our website. This financial relationship might influence how products are displayed, yet it does not impact the integrity and thoroughness of our information and evaluations. Note that we do not encompass every available financial product or offer.

Commitment to Editorial Integrity

Our reviews are exclusively authored by our editorial staff, reflecting their own views. These insights remain unswayed by our sponsors. At TheEnquirer, we adhere to stringent principles of editorial independence and fairness to ensure unbiased content..

Expert Verified

Expert Verified

How Does TheEnquirer Ensure Expert-Verified Content?

How Does TheEnquirer Ensure Expert-Verified Content?