Equity Release Pitfalls: Avoid Common Retirement Mistakes

Common pitfalls include accruing high interest over time and impacting eligibility for means-tested benefits. We see awareness of these issues as critical for homeowners.

Last Updated: 15 Apr 2025

Fact Checked

Our team recently fact checked this article for accuracy. However, things do change, so please do your own research.

Katherine Read is a financial writer known for her work on financial planning and retirement finance, covering equity release, lifetime mortgages, home reversion, retirement planning, SIPPs, pension drawdown, and interest-only mortgages.

Bert Hofhuis Is a Founder & Entrepreneur Simplifying the Complexities of Later Life Planning. He Navigates the Intricacies of Equity Release, Lifetime Mortgages, Reverse Mortgages, and Wealth Management With Clarity and Expertise.

In his long professional career, Bert has worked with multinational companies and governments, consulting on various financial and logistical projects in Africa, Europe and Asia.

He founded The Enquirer with a team of experienced finance writers and experts to help demystify topics such as equity release, lifetime mortgages, home reversions and retirement interest only mortgages, for people like himself.

Paul Derek Sawyer is an esteemed external compliance consultant in equity release, specializing in lifetime mortgages and home reversion plans. With over 20 years of experience, he expertly navigates the complexities of Equity Release Council standards and regulations.

His focus is on ensuring ethical lending practices and safeguarding consumer interests. Renowned for his expertise in financial services compliance, risk management, and audit, Paul is dedicated to promoting financial security for the elderly.

Bert Hofhuis Is a Founder & Entrepreneur Simplifying the Complexities of Later Life Planning. He Navigates the Intricacies of Equity Release, Lifetime Mortgages, Reverse Mortgages, and Wealth Management With Clarity and Expertise.

In his long professional career, Bert has worked with multinational companies and governments, consulting on various financial and logistical projects in Africa, Europe and Asia.

He founded The Enquirer with a team of experienced finance writers and experts to help demystify topics such as equity release, lifetime mortgages, home reversions and retirement interest only mortgages, for people like himself.

TheEnquirer Promise

Expert Verified

Avoiding Equity Missteps: Identify Common Pitfalls, Their Consequences & Preventive Measures. But Are There Hidden Traps?

Key Takeaways

Common pitfalls of equity release include accruing high amounts of compound interest, reducing inheritance for heirs, and restrictions on moving or selling your home.

To avoid, seek independent financial and legal advice, choose a plan with a no negative equity guarantee, and discuss your decision with family members.

There can be hidden costs, such as setup fees, legal fees, valuation fees, and potentially early repayment charges, so it’s crucial to ask about all possible fees upfront.

It can significantly impact your family and heirs by reducing the amount of inheritance you can leave behind, so it’s important to involve them in your decision-making process.

It can affect your state benefits, as the money received may be counted as income or assets, potentially affecting your eligibility for means-tested benefits.

Embarking your later-life financial journey? Understanding the Equity Release Pitfalls should be your first step.

From the compound interest that seems innocuous but grows stealthily over time to the unexpected effects on future inheritances, unlocking property value is not a decision to be made lightly.

What You'll Learn in This Article:

In this comprehensive guide, we aim to demystify these complexities, offering insights into potential risks and providing tips for a more informed and strategic approach.

Who Offers the Lowest Rates in 2025?

Discover the Lowest Rates & Save

Request a FREE call back & discover:

Who offers the LOWEST rates available on the market.

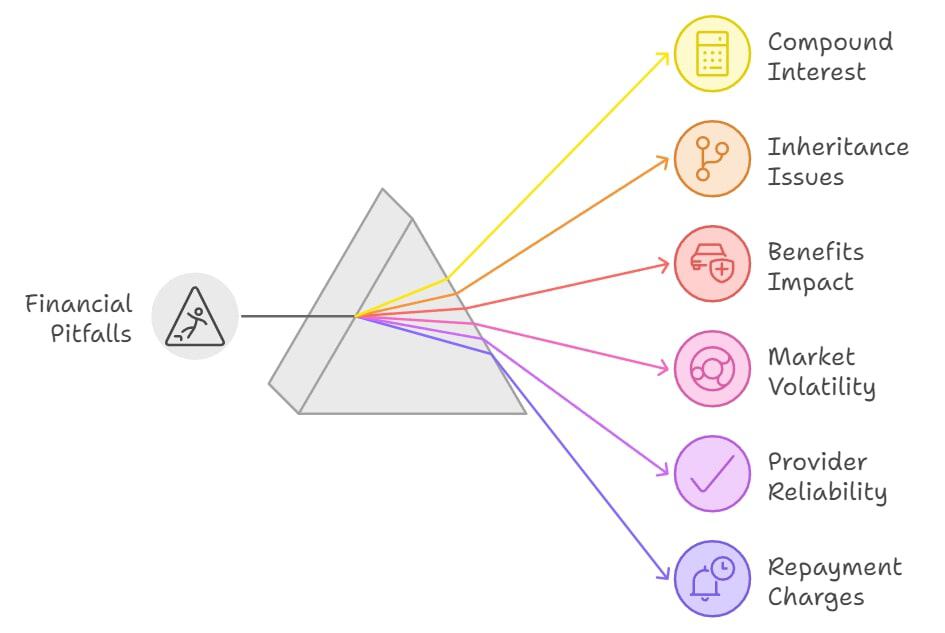

Before opting to release equity it's vital to be aware of any potential that you may encounter, such as compound interest, diminished inheritance, impact on benefits, market volatility, and unreliable providers.

Here’s a breakdown of the 7 highest-risk pitfalls to be aware of.

#1. Tackling Compound Interest

Interest that's compounded, especially over extended periods, can significantly increase the amount owed.

This can lead to a situation where the owed amount becomes considerably higher than initially borrowed.

Specialist's Suggestion: Plans allow for frequent interest repayments. It's essential to understand how the interest is calculated and compounded to manage the long-term implications.1

#2. Diminished Inheritance

Leveraging the equity in your home can dramatically alter or diminish the legacy you leave behind for your heirs.

Top Recommendation: Hold transparent discussions with potential heirs and consider a designated portion for inheritance. Evaluate other financial solutions if preserving inheritance is a priority.

#3. Impact Your Benefits

An influx in liquidity or assets from releasing equity can impact thresholds for various state benefits,2 possibly resulting in a loss of crucial financial support.

Insider's Suggestion: Consult with professionals experienced in benefits and entitlements who can guide how it might affect your specific situation.

#4. Property Market Volatility

If property values decrease, the equity secured against the property might become disproportionate, leading to potential negative equity situations.

Expert Insight: Ensure your agreement has protective clauses against negative equity scenarios due to Equity Release Council membership. Staying informed on property market trends can also help in making informed decisions.

#5. Unreliable Providers

As the sector grows, so does the likelihood of encountering providers without transparent or ethical practices, leading to unfavourable terms or hidden costs.

Key Advice: Opt for well-reviewed, accredited providers with a track record of reliability. Rely on independent financial consultants to vet potential providers and guide your choices.

#6. Early Repayment Charges

Some plans come with hefty early repayment charges, which could make it expensive if you wish to pay off the loan ahead of schedule.3

Prudent Pointer: Thoroughly understand any penalties or charges associated with your scheme. If foreseeing an early repayment, seek plans with minimal or no such fees.

#7. Limited Future Financial Options

After committing to a plan you might find your options limited should you wish to secure further loans or make significant financial changes in the future.

Wise Warning: Before finalising your scheme, consider your long-term financial plans, to make sure that your decision doesn't unduly restrict future financial flexibility.

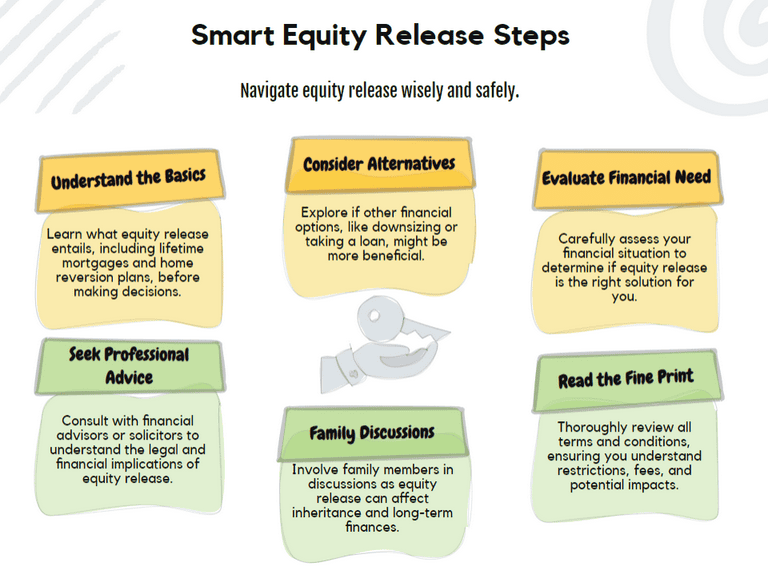

How To Approach Equity Release with Caution & Awareness

Before embarking on this financial journey, it's crucial to tread with caution and an informed perspective.

Here are 5 essential tips:

Educate Yourself: As the sector is ever-evolving, and driven by regulatory shifts and market dynamics, it's also essential to stay updated with the latest trends and changes.

Seek Independent Financial Advice: Engaging with an independent financial advisor can offer invaluable insights. Their detachment from specific providers ensures you receive unbiased recommendations.

Communicate with Your Family: Using property value can have ramifications on the inheritance you might leave behind. It's essential to involve family members in the discussion, ensuring everyone's expectations are aligned. This can also bring forth varied viewpoints, offering a more holistic perspective.

Read the Fine Print: Before committing, go through every detail of the agreement. Understand the associated fees, interest rate structures, and any potential penalties. If any clauses seem unclear, don't hesitate to ask for clarity. It's always better to be proactive at this stage than to encounter surprises later.

Have a Long-term Strategy: While releasing equity might seem beneficial in the present, it's crucial to think long-term. Consider possible future scenarios, such as wanting to move homes or needing to repay the amount earlier than anticipated. Opting for plans that offer flexibility in such instances can prove beneficial in the long run.

How Does the Equity Release Council Help Mitigate Potential Pitfalls?

The Equity Release Council (ERC)4 plays a key role in mitigating pitfalls by setting high standards, protecting consumers, providing education and awareness, dispute resolution, as well as keeping a finger on the pulse of market development.

Setting High Standards: The ERC establishes rigorous standards that members must uphold, ensuring professionalism and ethical behaviour in the industry.

Protection for Consumers: The Council champions the No Negative Equity Guarantee, which ensures homeowners never owe more than the value of their home.

Education and Awareness: The ERC provides a wealth of resources and information for consumers to understand the topic better.

Dispute Resolution: If there's a disagreement between a consumer and a provider, the ERC can provide guidance or even mediation.

Regularly Updating Guidelines: The market evolves, and the ERC adapts its guidelines accordingly, ensuring current practices always have the consumer's best interest at heart.

Common Questions

In What Scenarios Is Equity Release Not Advisable?

Using property value may not be advisable if you're looking to preserve the full value of your property for inheritance if you anticipate a significant increase in your income soon, or if you're planning to move or downsize shortly.

It's essential to assess the impact on your tax position and benefits entitlements as well.

How Does Equity Release Impact My Ability to Move or Downsize My Property in the Future?

While many plans allow homeowners to move and transfer the plan to a new property, there are conditions to meet.

It's essential to ensure the new property is acceptable to the provider.

Downsizing might be possible, but you could incur early repayment charges if you don't transfer the plan.

Can I Add Another Person to My Plan After It Has Started, Such as a New Spouse or Partner?

Typically, adding someone to an existing plan is not straightforward and often requires repaying the current plan and taking out a new one that includes the additional person.

It's crucial to consult your provider or an independent financial advisor for specifics.

Are There Any Measures I Can Take to Preserve a Portion of My Property’s Value for Inheritance?

Yes, many plans offer inheritance protection or the ability to ring fence a portion of the property's value to ensure a guaranteed inheritance for your heirs, regardless of how much interest accumulates.

How Does Equity Release Affect My Tax Position?

Funds received are tax-free. However, if invested, the returns may be subject to taxation.

Regarding inheritance tax, the property's value (minus the loan amount) is considered for tax calculations when you pass away.

Can I Repay the Equity Release Loan Early? If So, What Penalties or Charges Might I Incur?

Products permit early loan settlement. However, the cost implications, like early repayment penalties, hinge on the product's conditions and the loan's active duration.

In Conclusion

Equity release offers homeowners a pathway to unlock their property's value, but it's essential to tread with caution.

From affecting inheritance and tax positions to potential repercussions on means-tested benefits and long-term care options, the implications are vast.

While it can be a beneficial tool, it's vital to be well-versed in equity release pitfalls.

How Does TheEnquirer Ensure Expert-Verified Content?

At TheEnquirer, the integrity and precision of our information is paramount.

Being "expert verified" signifies that our review panel has meticulously assessed each article for precision and comprehensibility. This panel is made up of seasoned professionals in compliance is dedicated to guaranteeing that our content remains impartial and well-informed.

Their rigorous evaluations compel us to maintain a standard of excellence, ensuring that the information we provide is both reliable and of the highest quality.

Financial Guidance Disclaimer for TheEnquirer Readers

Understanding Our Revenue Stream

TheEnquirer operates as an autonomous, ad-supported online platform. Our mission is to furnish you with essential tools and insights for wiser financial choices, granting access to our interactive resources and impartial journalism at no cost.

Please note that while our content is educational, it is not meant as specific financial advice and should not be the only factor in your decision-making. We advise seeking personalized advice from a financial expert to cater to your unique investment needs.

How We Generate Income

Our earnings come from endorsements for products featured on our website. This financial relationship might influence how products are displayed, yet it does not impact the integrity and thoroughness of our information and evaluations. Note that we do not encompass every available financial product or offer.

Commitment to Editorial Integrity

Our reviews are exclusively authored by our editorial staff, reflecting their own views. These insights remain unswayed by our sponsors. At TheEnquirer, we adhere to stringent principles of editorial independence and fairness to ensure unbiased content..

Expert Verified

Expert Verified

How Does TheEnquirer Ensure Expert-Verified Content?

How Does TheEnquirer Ensure Expert-Verified Content?