Horror stories often involve unexpected debt accumulation and impacts on inheritance. We see these as cautionary tales underscoring the need for thorough understanding and planning.

Last Updated: 11 Apr 2025

Fact Checked

Our team recently fact checked this article for accuracy. However, things do change, so please do your own research.

Katherine Read is a financial writer known for her work on financial planning and retirement finance, covering equity release, lifetime mortgages, home reversion, retirement planning, SIPPs, pension drawdown, and interest-only mortgages.

Bert Hofhuis Is a Founder & Entrepreneur Simplifying the Complexities of Later Life Planning. He Navigates the Intricacies of Equity Release, Lifetime Mortgages, Reverse Mortgages, and Wealth Management With Clarity and Expertise.

In his long professional career, Bert has worked with multinational companies and governments, consulting on various financial and logistical projects in Africa, Europe and Asia.

He founded The Enquirer with a team of experienced finance writers and experts to help demystify topics such as equity release, lifetime mortgages, home reversions and retirement interest only mortgages, for people like himself.

Paul Derek Sawyer is an esteemed external compliance consultant in equity release, specializing in lifetime mortgages and home reversion plans. With over 20 years of experience, he expertly navigates the complexities of Equity Release Council standards and regulations.

His focus is on ensuring ethical lending practices and safeguarding consumer interests. Renowned for his expertise in financial services compliance, risk management, and audit, Paul is dedicated to promoting financial security for the elderly.

Bert Hofhuis Is a Founder & Entrepreneur Simplifying the Complexities of Later Life Planning. He Navigates the Intricacies of Equity Release, Lifetime Mortgages, Reverse Mortgages, and Wealth Management With Clarity and Expertise.

In his long professional career, Bert has worked with multinational companies and governments, consulting on various financial and logistical projects in Africa, Europe and Asia.

He founded The Enquirer with a team of experienced finance writers and experts to help demystify topics such as equity release, lifetime mortgages, home reversions and retirement interest only mortgages, for people like himself.

TheEnquirer Promise

Expert Verified

Learning from Mistakes: Read About Real-Life Equity Release Mishaps, Their Causes & Lessons. But Could You Avoid Them?

Key Takeaways

Common themes in equity release horror stories include unexpectedly high interest accumulation, an impact on inheritance, and difficulties in changing terms or moving homes.

To avoid becoming a cautionary tale, seek advice from a qualified financial advisor, understand the long-term implications, and choose products approved by the Equity Release Council.

Horror stories are relatively rare, especially with products that comply with ERC standards, but they can occur, often owing to a lack of understanding or poor advice.

Lessons include the importance of understanding the compound interest effect, the value of early consultation with family, and the necessity of reading and understanding all terms before agreement.

Regulators and the ERC respond by enforcing strict standards, requiring transparent advice and clear terms, and implementing safeguards like the No Negative Equity guarantee to protect consumers.

Delving into equity release horror stories offers a unique perspective on the challenges some borrowers face when accessing the value in their homes.

What You'll Learn in This Article:

Through these tales, we aim to arm you with the knowledge to navigate this terrain wisely and make informed decisions that best serve your financial well-being.

This guide will shed some light on these horror stories and how to avoid similar situations.

Who Offers the Lowest Rates in 2025?

Discover the Lowest Rates & Save

Request a FREE call back & discover:

Who offers the LOWEST rates available on the market.

A Telegraph report from January 2025 covers the story of a man who found out that his dad had taken out an equity release loan and let the interest pile up for 12 years.1

By the time the man found out about the loan, his dad's £100,000 debt had doubled to £200,000.

What went wrong?

His dad had taken the loan to pay off credit card debt, but if he had talked to his kids first, they could have helped him out.

Instead, a third of their inheritance was lost, and one sibling had to buy the house to clear the debt.

In 2021, This Is Money reported on David and Joanne Horton, who had taken out a £384,000 equity release loan on their farm in 2008 to boost their pension.2

When Joanne tried to sell the farm in 2021, eight years after David died, she found out she needed almost £1 million to settle the debt.

What went wrong?

This huge amount was made up of about £500,000 in rolled-up interest and an Early Repayment Charge (ERC) of £96,000, triggered by a drop in the Bank of England’s base rate.

Plus, their old equity release plan did not have a feature that lets surviving partners repay the loan without penalties if the other partner dies or moves into care.

Equity Release Horror Story #3

Rosemary’s story, shared in a 2019 Guardian article, involves her parents taking out an equity release loan in the 1990s.3

When her mum, June, died in 2019, Rosemary was given just a month to move out of the house they shared.

What went wrong?

Unlike lifetime mortgages, which usually allow a year for selling the property after the last borrower dies, Rosemary’s parents had a home reversion agreement.

These deals often only give surviving tenants a month to leave so the property can be sold.

Rosemary did eventually get an extra two months to move out.

Also notable

In 1994, Rosemary's parents got £52,000 for a 90% stake in their home, which would now be worth nearly £1 million.

Equity Release Horror Story #4

Roy and Jean Tamplin’s story, reported by This Is Money in 2015, came to a head when they decided to move into care in 2014.4

The couple found out they needed to repay the £119,000 they owed on their equity release loan and also had to pay a £16,430 Early Repayment Charge (ERC) for ending the loan early.

What went wrong?

Their agreement said the ERC would be waived if both partners moved into care simultaneously.

However, the provider ruled that only Roy needed care, while Jean was considered healthy enough to stay at home, meaning they had to pay the ERC if they moved out together.

What Are Equity Release Horror Stories Caused By?

Equity release horror stories are often caused by misunderstanding a number of product features.

While this financial tool can offer relief, it can also lead to unexpected pitfalls if not approached with caution.

Here are 4 factors that may lead to bad experiences with equity release.

#1. Compounding Interest

Interest on borrowed money, if misunderstood, can exponentially amplify the owed amount, turning manageable loans into crippling debts:

Problem: Compound interest on equity release loans can cause large debts because interest is charged on both the original loan amount and any accumulated interest, causing the debt to grow exponentially over time if not repaid.

Solution: Before opting for an equity release, use an interest calculator to project long-term costs.5 Understand the difference between fixed and variable rates and the implications of compounding interest over the years.

#2. Rigidity of Agreements

While a particular equity release agreement might seem beneficial at first, the terms of an agreement can sometimes restrict future financial manoeuvres.

Problem: It may be possible to be lured by an attractive financial offer, only to get stuck in an equity release plan with inflexible terms. When the market shifts and offers better interest rates, you might find yourself unable to refinance or adapt to the changing landscape.

Guidance: Review the agreement terms meticulously. Ensure that the plan allows for flexibility, such as the ability to switch to a better rate or make ad hoc repayments without excessive penalties. (Luckily, all new lifetime mortgage plans approved by the Equity Release Council now allow partial penalty-free repayments.)

#3. Diminished Inheritance

Equity release, if not managed prudently, can significantly diminish the legacy homeowners intend to leave behind.

Problem: You may hope to preserve a substantial inheritance by releasing only 40% of your property's equity. However, after two decades of accumulating interest, the outstanding debt to the equity release company grows to consume 80% of the property's value.

Recommendation: Look for a plan that allows you to ring-fence a portion of your property for your heirs and beneficiaries. Regularly reviewing the plan can also help ensure it aligns with your inheritance goals.

#4. Hidden Charges & Fees

Beneath the surface of a seemingly straightforward equity release lie hidden costs that can silently pile up:

Problem: You may start by borrowing £150,000 through equity release. However, costs and fees—from administrative costs to early repayment penalties—may add significantly to the initial debt.

Tip: Transparency is key. Request a detailed breakdown of all potential charges from the equity release provider, including any conditions that might trigger additional fees in the future.

The Equity Release Council: The ERC is fundamentally committed to upholding rigorous standards of conduct and practice. Beyond representation, its core mission is to ensure consumers receive fair and transparent services. To this end, all member organisations are obliged to adhere to stringent standards.8

Financial Conduct Authority: Serving as the UK's chief regulatory body for financial entities, the FCA maintains a vigilant eye over the vast landscape of the financial services sector. This oversight guarantees that equity release firms uphold values of integrity, and clarity, and always act in the client's best interests.

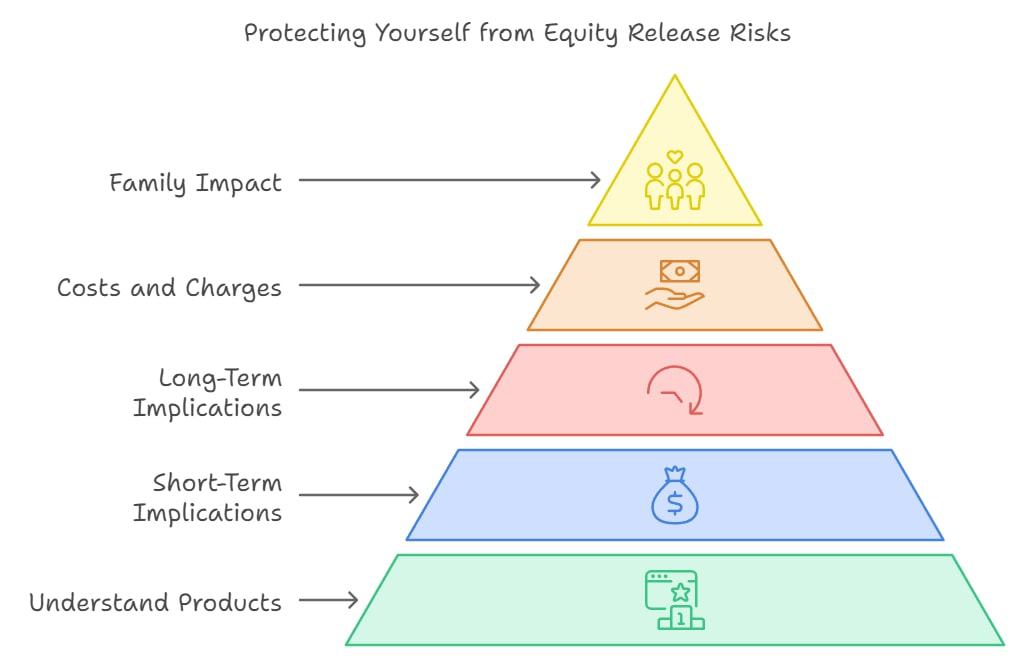

How Can You Protect Yourself?

To protect yourself from similar situations, it is vital to do thorough research, and get to grips with all available plans, long- and short-term implications, costs, charges, and the potential impact on your family.

Here is a breakdown:

Understand Different Products: Familiarise yourself with the various products available, such as lifetime mortgages and home reversion plans, as each has its pros and cons.

Short-term Implications: Consider how equity release will impact your current finances. You may face a reduction in monthly income if you're drawing down from a lump sum or regular payments.

Long-Term Implications: Realise that equity release could affect your eligibility for state benefits, tax position, and the amount you could leave as an inheritance.

Costs and Charges: Beyond the interest rate, there can be other charges such as arrangement fees, valuation fees, and early repayment charges. Ensure you have a clear picture of all costs involved.

Consider the Impact on Your Family: Equity release can reduce the value of your estate. Discuss your intentions with your family, as it may affect their inheritance.

Which Other Organisations Can Help?

Besides the FCA and the ERC, there are several other bodies in the UK designed to safeguard consumers and maintain the integrity of the equity release industry:

Solicitors for the Elderly (SFE):9 This independent, national organisation consists of lawyers who specialise in providing legal advice to older and vulnerable individuals. They address matters ranging from equity release to estate planning and wills.

Age UK:10 As the UK's leading charity dedicated to aiding those in their later years, Age UK offers advice and resources on a multitude of topics, including equity release, retirement planning, and more.

The Pensions Advisory Service (TPAS):11 A free-to-use service, TPAS provides information and guidance on all pension-related topics, including the interplay between pensions and equity release.

Citizens Advice:12 This nationwide service offers free, independent advice on a plethora of financial matters, equity release being one of them. They aim to help people understand their rights and navigate complex financial decisions.

The National Association of Property Buyers (NAPB):13 While their primary focus is on quick property sales, they also provide guidance and uphold standards related to property-based financial decisions, including equity release.

The Society of Later Life Advisers (SOLLA):14 SOLLA aids consumers in finding trusted financial advisers who specialise in the financial needs of older individuals. Their members are trained to understand the specific requirements related to later-life planning, including equity release.

Common Questions

How Long Does the Equity Release Process Usually Take?

The process can vary depending on the provider and individual circumstances, but typically, it takes between 6 to 12 weeks from the initial inquiry to funds release.

However, some cases can be quicker, while others might take longer.

Not necessarily. While there are inherent risks, many schemes, especially those regulated by the FCA and members of the ERC, have safety measures in place.

However, it's crucial to understand the terms and seek professional advice before committing.

How Can I Safeguard Myself Against Negative Equity?

Choose plans that have a "no negative equity guarantee". This ensures that you'll never owe more than the value of your home, protecting both you and your heirs from excessive debt.

What Are the Hidden Costs & Fees to Watch Out For?

Some potential hidden costs include early repayment charges, administrative fees, valuation fees, and setup charges.

Always request a full breakdown of costs before proceeding.

Can I Change My Mind After Taking Out Equity Release?

While you can repay an equity release plan early, it may come with significant early repayment charges.

It's essential to understand these potential penalties before finalizing any agreement.

Is It Possible to Transfer an Equity Release to a New Property if I Move?

Most equity release plans, especially lifetime mortgages, allow for portability, meaning they can be transferred to a new property, subject to the new property meeting the lender's criteria.

In Conclusion

Equity release is a tool that can offer financial flexibility in one's later years, but it's not without its intricacies.

By understanding the potential pitfalls and arming oneself with knowledge, one can navigate this complex terrain more confidently and make decisions that align well with your financial goals to avoid experiencing a real-life equity release horror story.

Editorial Note: This content has been independently collected by the team at The Enquirer and is offered on a non-advised basis. The Enquirer may earn a commission on sales made from partner links on this page, but that does not affect our editors’ opinions or evaluations. Learn more about our editorial guidelines.

How Does TheEnquirer Ensure Expert-Verified Content?

At TheEnquirer, the integrity and precision of our information is paramount.

Being "expert verified" signifies that our review panel has meticulously assessed each article for precision and comprehensibility. This panel is made up of seasoned professionals in compliance is dedicated to guaranteeing that our content remains impartial and well-informed.

Their rigorous evaluations compel us to maintain a standard of excellence, ensuring that the information we provide is both reliable and of the highest quality.

Financial Guidance Disclaimer for TheEnquirer Readers

Understanding Our Revenue Stream

TheEnquirer operates as an autonomous, ad-supported online platform. Our mission is to furnish you with essential tools and insights for wiser financial choices, granting access to our interactive resources and impartial journalism at no cost.

Please note that while our content is educational, it is not meant as specific financial advice and should not be the only factor in your decision-making. We advise seeking personalized advice from a financial expert to cater to your unique investment needs.

How We Generate Income

Our earnings come from endorsements for products featured on our website. This financial relationship might influence how products are displayed, yet it does not impact the integrity and thoroughness of our information and evaluations. Note that we do not encompass every available financial product or offer.

Commitment to Editorial Integrity

Our reviews are exclusively authored by our editorial staff, reflecting their own views. These insights remain unswayed by our sponsors. At TheEnquirer, we adhere to stringent principles of editorial independence and fairness to ensure unbiased content..

Expert Verified

Expert Verified

How Does TheEnquirer Ensure Expert-Verified Content?

How Does TheEnquirer Ensure Expert-Verified Content?