Equity Release Criteria: Qualify for Your Retirement Plan

Eligibility for equity release in the UK typically requires being over 55 years old, owning a property of sufficient value, and meeting the lender's specific criteria, aimed at homeowners looking to access their home's equity.

Last Updated: 11 Apr 2025

Fact Checked

Our team recently fact checked this article for accuracy. However, things do change, so please do your own research.

Katherine Read is a financial writer known for her work on financial planning and retirement finance, covering equity release, lifetime mortgages, home reversion, retirement planning, SIPPs, pension drawdown, and interest-only mortgages.

Bert Hofhuis Is a Founder & Entrepreneur Simplifying the Complexities of Later Life Planning. He Navigates the Intricacies of Equity Release, Lifetime Mortgages, Reverse Mortgages, and Wealth Management With Clarity and Expertise.

In his long professional career, Bert has worked with multinational companies and governments, consulting on various financial and logistical projects in Africa, Europe and Asia.

He founded The Enquirer with a team of experienced finance writers and experts to help demystify topics such as equity release, lifetime mortgages, home reversions and retirement interest only mortgages, for people like himself.

Paul Derek Sawyer is an esteemed external compliance consultant in equity release, specializing in lifetime mortgages and home reversion plans. With over 20 years of experience, he expertly navigates the complexities of Equity Release Council standards and regulations.

His focus is on ensuring ethical lending practices and safeguarding consumer interests. Renowned for his expertise in financial services compliance, risk management, and audit, Paul is dedicated to promoting financial security for the elderly.

Bert Hofhuis Is a Founder & Entrepreneur Simplifying the Complexities of Later Life Planning. He Navigates the Intricacies of Equity Release, Lifetime Mortgages, Reverse Mortgages, and Wealth Management With Clarity and Expertise.

In his long professional career, Bert has worked with multinational companies and governments, consulting on various financial and logistical projects in Africa, Europe and Asia.

He founded The Enquirer with a team of experienced finance writers and experts to help demystify topics such as equity release, lifetime mortgages, home reversions and retirement interest only mortgages, for people like himself.

TheEnquirer Promise

Expert Verified

Qualifying for Equity: Understand the Criteria, Eligibility & Requirements. But What Factors Could Disqualify You?

Key Takeaways

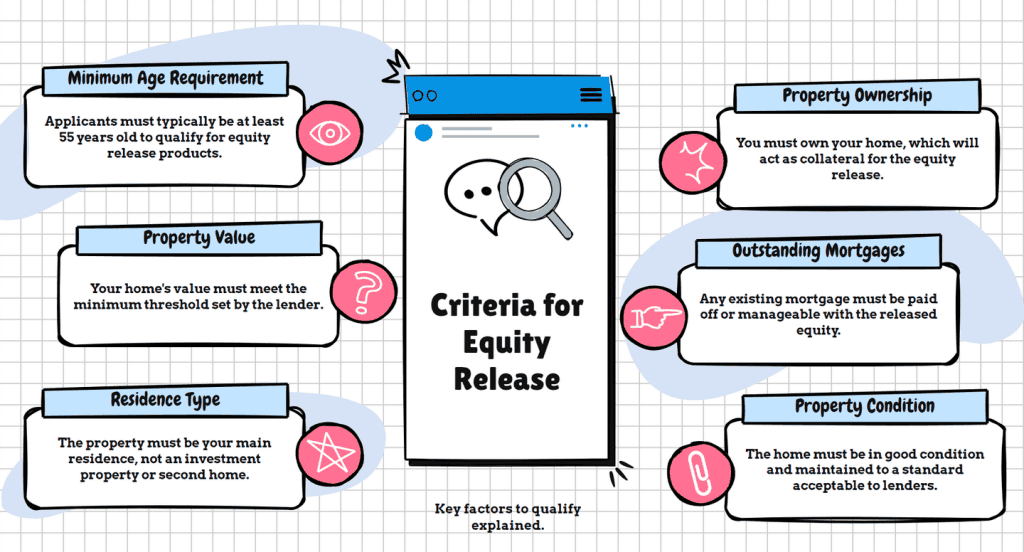

Basic eligibility criteria for equity release include being at least 55 years old (60 for some plans), owning a property in the UK, and having a minimum property value, often around £70,000.

Your property type affects eligibility; it must be in good condition and of a type that the provider is willing to accept, which can vary between lenders.

There are age restrictions for applicants; the minimum age is typically 55 years old, but better terms may be available for older applicants.

Your health can impact it, with some providers offering enhanced terms for those with certain health conditions or lifestyles that could reduce life expectancy.

You can apply with an existing mortgage, but you must use the funds to pay off the existing mortgage first, freeing the property from previous claims.

Have you wondered if equity release criteria could hold you back from unlocking your property’s wealth?

You’re not alone.

This criteria not only determines eligibility but also influences the terms and potential benefits you obtain from your provider.

So make sure you’re aware of what’s involved and what can be done to improve your chances.

What You'll Learn in This Article:

This article sheds light on the essential prerequisites and guidelines of equity release, equipping potential borrowers with the knowledge to navigate this path with confidence and clarity.

Who Offers the Lowest Rates in 2025?

Discover the Lowest Rates & Save

Request a FREE call back & discover:

Who offers the LOWEST rates available on the market.

While the specific minimum property value can vary between providers, generally, your property must be worth at least £70,000.2

Your property’s value is crucial as it determines how much equity you can release.

Is There a Minimum Equity?

Yes, most providers have a minimum release amount of £10,000.3

What’s the Maximum Loan-to-Value Ratio?

The maximum loan-to-value (LTV) ratio varies among providers and depends on factors such as your age, any health conditions you may have, and your property’s value.

Typically

The LTV ratio for equity release ranges between 20% and 60%,4 The older you are, the higher the percentage you can borrow.

The maximum loan amount you can get from an equity release scheme largely varies between what you qualify for and what providers will offer.

For example, a healthy 65-year-old with a property worth £300,000 may be able to release up to £105,000, based on a maximum LTV ratio of 35%.*

*These figures are for indicative purposes only.

What Are the Other Eligibility Criteria?

Other criteria include:

Your property must be in the UK and of standard construction.

You must live in the property as your primary residence.

You should be up-to-date on any existing mortgage repayments.

The property should be in a good state of repair.

Criteria for Your Property to Qualify for Equity Release

Not all properties are automatically eligible, and there are additional property-specific requirements that must be met.

Here are some common criteria and considerations:

If You Have a Mortgage: If you have an existing mortgage, your property can still be considered for equity release, but the funds must first be used to settle your existing mortgage. Any excess funds can be used as you see fit.

On Freehold Property: Freehold properties, where you own both the land and building, are typically suitable for equity release. The value of your freehold property will largely determine the amount you can release.

On Commonhold Property: Commonhold properties, where individual units within a complex are owned while shared areas are communal, may be considered. The provider will likely want to review the specifics of the commonhold agreement.

On Commercial Property: Commercial properties typically don't qualify for standard equity release. However, semi-commercial properties, like a shop with a residence above, may be considered by some providers.

On Buy-to-let Property: Some products cater specifically to buy-to-let properties. The terms for these products can differ from traditional schemes.

On Rented Property: Equity release isn’t available for rented properties, as the property needs to be your primary residence.

With a Tenant or Lodger: Having a tenant or lodger may complicate the process. Some providers may require the tenant or lodger to sign away their occupancy rights to approve the release.

Property Title Deeds: Your property title deeds should be clear and available for review. These documents will be essential during the application process, confirming property ownership. Furthermore, the deed can have no more than 2 people listed.

Japanese Knotweed: The presence of Japanese Knotweed can hamper your equity release eligibility due to its potentially damaging nature - a professional removal plan may be needed before your application can proceed.

Personal Criteria to Qualify for Equity Release

When it comes to personal criteria, your individual circumstances play a crucial role.

These conditions often hinge on your age, health, and financial standing, amongst others.

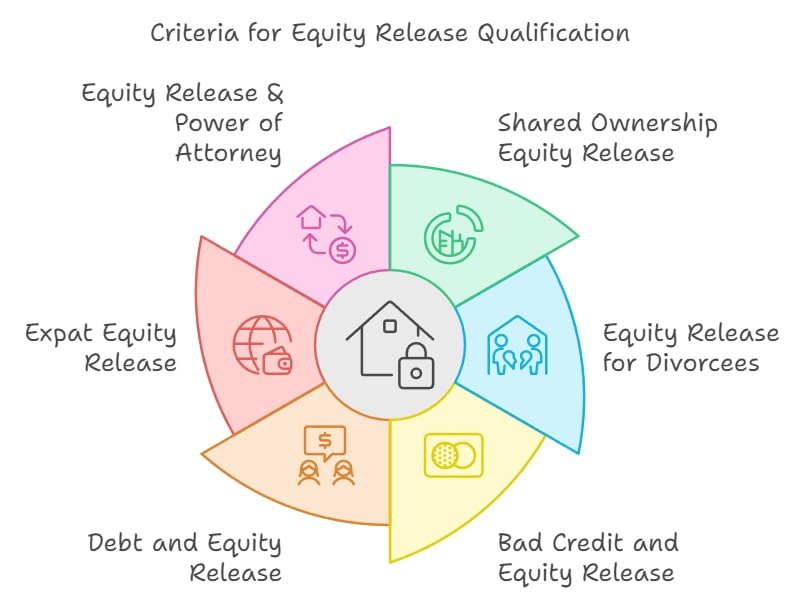

Shared Ownership Equity Release

Shared ownership properties can qualify for equity release.

However

There can’t be more than 2 people on your property title deed and both owners must meet age qualification criteria.

While credit history may not be a significant factor, providers may be cautious if there's evidence of recent adverse credit issues, like bankruptcy or defaults.

However

Each provider has its own criteria, so it's worth discussing this with a financial advisor.

Many people use equity release to consolidate and pay off their debts.

However, if you have mortgage debt, it’ll need to be an amount that can be paid off using your released cash.

Do Expats Qualify For Equity Release?

Yes, expat homeowners can qualify for equity release, but the options may be limited compared to UK residents.

The property in question must be in the UK, and you may need to provide proof of your ongoing connection to the property because it must be your primary residence.

How Equity Release & Power of Attorney Can Work Together

Power of Attorney (PoA) allows someone to act on your behalf if you're unable to make decisions.

A person with a registered PoA can apply for equity release on your behalf, provided they show that it’s in your best interest.

Common Questions

What Are the Most Important Criteria to Meet for Equity Release?

The most important criteria for equity release include being at least 55 years old, owning a property worth a minimum of £70,000, and being a UK resident.

Other factors like property type, financial status, and health conditions also play a role.

What Are the Criteria for Lifetime Mortgage?

The criteria for lifetime mortgages is as mentioned above since it’s the most popular type of plan.

This includes the minimum age of 55, owning a qualifying property, and ensuring your property is your main residence.

Do Home Reversion Criteria Differ From Lifetime Mortgage Equity Release Criteria?

Home Reversion plans, another form of equity release, usually require you to be at least 65 years old (depending on the provider).

Otherwise, the basic criteria are similar.

Where Do I Find an Equity Release Criteria Calculator?

These costs can be substantial, so it's important to consider this before proceeding.

Can Releasing Equity From Your Property Affect Your Eligibility for Government Benefits?

Yes, releasing equity can affect your eligibility for means-tested benefits, as it could be deemed as increasing your income.

It's crucial to seek advice before proceeding if you receive these benefits.

Do Equity Release Plans Have Early Repayment Fees?

Plans usually have early repayment fees.

This makes it important to consider your long-term plans and discuss potential scenarios with your provider before signing a contract.

Who Must Manage Property Maintenance During an Equity Release Plan?

You’re responsible for keeping the property in good condition throughout the plan.

Failure to do so can result in penalties.

How Does Inflation Influence Equity Release Loans?

Inflation can have a significant impact, particularly if you have a lifetime mortgage, the most common type of scheme.

With a lifetime mortgage, you borrow a percentage of your home's value at a usually fixed or ocassionally variable capped interest rate.

The loan, plus accrued interest, is repaid when you die or move into long-term care.

If you choose not to make repayments, the interest 'rolls up' and is added to the loan. This is where inflation comes into play.

In Conclusion

Equity release, involving plans like lifetime mortgages and home reversion, is governed by numerous criteria such as age, property value, and financial health.

The decision can impact your estate's value, government benefits, and property upkeep responsibilities.

Complexities arise with bad credit, expat status, unconventional property types, and inflation.

Editorial Note: This content has been independently collected by the SovereignBoss team and is offered on a non-advised basis. SovereignBoss may earn a commission on sales made from partner links on this page, but that doesn’t affect our editors’ opinions or evaluations. Learn more about our editorial guidelines.

How Does TheEnquirer Ensure Expert-Verified Content?

At TheEnquirer, the integrity and precision of our information is paramount.

Being "expert verified" signifies that our review panel has meticulously assessed each article for precision and comprehensibility. This panel is made up of seasoned professionals in compliance is dedicated to guaranteeing that our content remains impartial and well-informed.

Their rigorous evaluations compel us to maintain a standard of excellence, ensuring that the information we provide is both reliable and of the highest quality.

Financial Guidance Disclaimer for TheEnquirer Readers

Understanding Our Revenue Stream

TheEnquirer operates as an autonomous, ad-supported online platform. Our mission is to furnish you with essential tools and insights for wiser financial choices, granting access to our interactive resources and impartial journalism at no cost.

Please note that while our content is educational, it is not meant as specific financial advice and should not be the only factor in your decision-making. We advise seeking personalized advice from a financial expert to cater to your unique investment needs.

How We Generate Income

Our earnings come from endorsements for products featured on our website. This financial relationship might influence how products are displayed, yet it does not impact the integrity and thoroughness of our information and evaluations. Note that we do not encompass every available financial product or offer.

Commitment to Editorial Integrity

Our reviews are exclusively authored by our editorial staff, reflecting their own views. These insights remain unswayed by our sponsors. At TheEnquirer, we adhere to stringent principles of editorial independence and fairness to ensure unbiased content..

Expert Verified

Expert Verified

How Does TheEnquirer Ensure Expert-Verified Content?

How Does TheEnquirer Ensure Expert-Verified Content?