Equity Release Interest Rates: Understanding Your Costs

Equity release interest rates vary by provider and market conditions. We recommend regularly checking rates as part of your research to find the most cost-effective solution.

Last Updated: 14 Apr 2025

Fact Checked

Our team recently fact checked this article for accuracy. However, things do change, so please do your own research.

Katherine Read is a financial writer known for her work on financial planning and retirement finance, covering equity release, lifetime mortgages, home reversion, retirement planning, SIPPs, pension drawdown, and interest-only mortgages.

Bert Hofhuis Is a Founder & Entrepreneur Simplifying the Complexities of Later Life Planning. He Navigates the Intricacies of Equity Release, Lifetime Mortgages, Reverse Mortgages, and Wealth Management With Clarity and Expertise.

In his long professional career, Bert has worked with multinational companies and governments, consulting on various financial and logistical projects in Africa, Europe and Asia.

He founded The Enquirer with a team of experienced finance writers and experts to help demystify topics such as equity release, lifetime mortgages, home reversions and retirement interest only mortgages, for people like himself.

Paul Derek Sawyer is an esteemed external compliance consultant in equity release, specializing in lifetime mortgages and home reversion plans. With over 20 years of experience, he expertly navigates the complexities of Equity Release Council standards and regulations.

His focus is on ensuring ethical lending practices and safeguarding consumer interests. Renowned for his expertise in financial services compliance, risk management, and audit, Paul is dedicated to promoting financial security for the elderly.

Bert Hofhuis Is a Founder & Entrepreneur Simplifying the Complexities of Later Life Planning. He Navigates the Intricacies of Equity Release, Lifetime Mortgages, Reverse Mortgages, and Wealth Management With Clarity and Expertise.

In his long professional career, Bert has worked with multinational companies and governments, consulting on various financial and logistical projects in Africa, Europe and Asia.

He founded The Enquirer with a team of experienced finance writers and experts to help demystify topics such as equity release, lifetime mortgages, home reversions and retirement interest only mortgages, for people like himself.

TheEnquirer Promise

Expert Verified

Interest Rate Insights: Understand Equity Release Rates, Their Fluctuations & Impact. But How Will They Affect Your Choice?

Key Takeaways

Equity release interest rates are calculated based on the loan amount, your age, property value, and market conditions, with the rate fixed at the outset for lifetime mortgages.

Factors include the Bank of England base rate, lender's funding costs, property value, and the borrower's age and health.

They are generally higher than traditional mortgage rates due to the lender not receiving repayments until the property is sold.

For lifetime mortgages, the interest rate is usually fixed for the life of the loan, but some products offer variable rates that can change over time.

To find the best rates, compare offers from multiple providers, consider using an independent adviser, and look for plans approved by the Equity Release Council.

As homeowners explore avenues for financial flexibility, grasping the nuances of equity release interest rates becomes vital.

Whether you're considering a lifetime mortgage or a home reversion scheme, understanding how these rates work and their potential impact is essential for a sound financial journey.

This article sheds light on the intricacies of these rates, their dynamics, and how they can shape your overall experience.

What You'll Learn in This Article:

This article demystifies the complexities surrounding equity release interest rates, offering insights into their dynamics and how they shape the overall equity release journey for homeowners.

Who Offers the Lowest Rates in 2025?

Discover the Lowest Rates & Save

Request a FREE call back & discover:

Who offers the LOWEST rates available on the market.

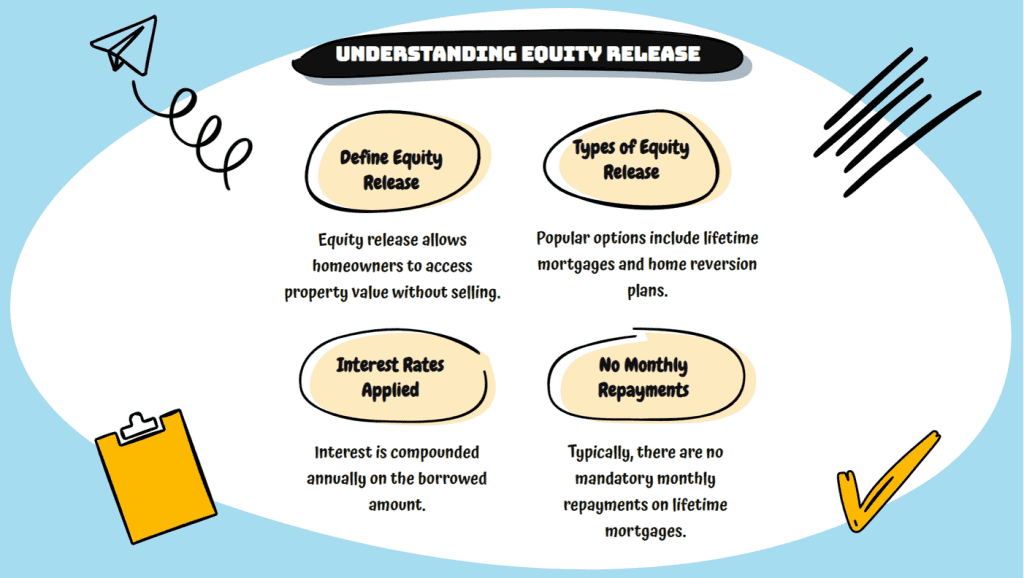

Home reversions entail a sale of your property to your lender, so there’s no interest since it’s not a loan.

Take note

The interest is compounded, meaning you not only pay interest on the initial loan but also on the accumulating interest, leading to a significant escalation in the overall amount owed.

Fixed vs Variable Rates

Products come with either fixed or variable rates.

A fixed rate remains constant throughout the loan term, offering certainty about the cost, while a variable rate can fluctuate based on market conditions.

However, all variable rate plans must have a "cap" or "collar" that sets a maximum limit on how high the rate can increase, as per an Equity Release Council-standard.1

Currently, all equity release schemes are offered with a fixed interest rate.

What Affects Interest Rates on Equity Release?

Several factors influence achieved interest rates, including market conditions, the loan-to-value (LTV) ratio, lender policies, property value, and your health.

Although

It’s essential to understand that lower rates don’t necessarily translate to the best offer; associated fees and loan terms also play a crucial role.

Average Equity Release Interest Rates in 2026

As of 2026, the Equity Release Council's Spring market report highlighted that the average equity release interest rates in the UK have fallen to 6.21% AER.

Additionally, data from Responsible Equity Release indicates a median rate of 6.19% AER. Rates can be influenced by market conditions and specific lender policies.

However, it's essential to note that personal circumstances and the selected equity release plan can impact the final rate you receive.

Current Equity Release Interest Rates Compared

Provider

Scheme Name

Monthly (Rate)The amount of interest due per period, as a proportion of the amount lent, deposited, or borrowed.

Pure Retirement

Age Partnership Classic Flexible Lump Sum 1

5.97%

Canada Life

Age Partnership Ultra Lite Fixed ERC

6.13%

Canada Life

Capital Select Ultra Lite Fixed ERC

6.16%

Aviva

Age Partnership Lifestyle Flexible Option, Fixed ERC

N/A

Canada Life

Age Partnership Ultra Lite Plus Fixed ERC

6.20%

Canada Life

Capital Select Ultra Lite Plus Fixed ERC

6.24%

Just Retirement

Age Partnership J1 Lump Sum (>25% Payments) Fixed ERC (Enhanced)

6.25%

Just Retirement

Age Partnership J1 Lump Sum (>25% Payments) Fixed ERC (Enhanced)

6.25%

Canada Life

Age Partnership Super Lite Fixed ERC

6.27%

Just Retirement

Age Partnership J2 Lump Sum (>25% Payments) Fixed ERC (Enhanced)

6.28%

Updated: 18.02.2025

Scenario

60 Year Old Single Male

£300k Property Value

£30k Release

*This rate was accurate upon publication. While we review our figures regularly, they may have changed since this article was last updated.

How to Compare & Reduce Rates of Interest

When comparing interest, look beyond the headline rate and consider the Annual Equivalent Rate (AER)2 for a more accurate reflection of the cost.

To potentially reduce your interest rate, consider making voluntary repayments, choosing a product with a lower interest rate, or negotiating with providers.

Can You Pay Back Interest on Equity Release Loans?

Yes, all lifetime mortgage schemes allow you to make voluntary interest repayments and a certain amount of the loan annually (usually 10%), without penalties.

This option can be beneficial for those looking to manage the escalation of interest over the years.

Equity Release Interest Calculator

Many online platforms provide calculators to help you estimate how much you could borrow and how the interest might accumulate over time.3

This is due to the long-term nature of equity release and the compounding of interest over time.

Can You Make Interest Payments on an Equity Release Plan?

Yes, you can make monthly interest payments, preventing the loan from increasing.

However

This depends on the specific terms of your plan, as your provider may charge a penalty if too much is paid within a certain time period.

Do Equity Release Interest Rates Differ Between Providers?

Yes, interest rates can vary considerably between providers.

Different lenders have different risk assessments, lending criteria, and market strategies, leading to variations in the interest rates they offer.

Do Interest Rates Vary in Different Areas of the UK?

While the location of your property can influence the amount you can release, it typically doesn’t impact the interest rate.

However, the local housing market conditions might indirectly affect the rates offered by lenders.

When Are Equity Release Rates Reviewed?

Fixed rates for equity release plans are set at the start and remain the same throughout the plan, but capped variable rates are reviewed.

Can a Person’s Health Impact Their Interest Rates Achieved?

Yes, some providers offer "enhanced" plans for those with certain health conditions or lifestyle factors, such as smoking.

These plans allow you to release more equity or potentially offer a reduced interest rate.

In Conclusion

Understanding interest in relation to equity release is essential due to their significant impact on the total cost of borrowing.

Over the past decade, rates have seen an evolution driven not just by market dynamics but also by regulatory changes and technological advancements in the financial sector.

With a comprehensive understanding of equity release interest rates, you can make an informed decision about using equity release to meet your financial goals.

Editorial Note: This content has been independently collected by the SovereignBoss team and is offered on a non-advised basis. SovereignBoss may earn a commission on sales made from partner links on this page, but that doesn’t affect our editors’ opinions or evaluations. Learn more about our editorial guidelines.

How Does TheEnquirer Ensure Expert-Verified Content?

At TheEnquirer, the integrity and precision of our information is paramount.

Being "expert verified" signifies that our review panel has meticulously assessed each article for precision and comprehensibility. This panel is made up of seasoned professionals in compliance is dedicated to guaranteeing that our content remains impartial and well-informed.

Their rigorous evaluations compel us to maintain a standard of excellence, ensuring that the information we provide is both reliable and of the highest quality.

Financial Guidance Disclaimer for TheEnquirer Readers

Understanding Our Revenue Stream

TheEnquirer operates as an autonomous, ad-supported online platform. Our mission is to furnish you with essential tools and insights for wiser financial choices, granting access to our interactive resources and impartial journalism at no cost.

Please note that while our content is educational, it is not meant as specific financial advice and should not be the only factor in your decision-making. We advise seeking personalized advice from a financial expert to cater to your unique investment needs.

How We Generate Income

Our earnings come from endorsements for products featured on our website. This financial relationship might influence how products are displayed, yet it does not impact the integrity and thoroughness of our information and evaluations. Note that we do not encompass every available financial product or offer.

Commitment to Editorial Integrity

Our reviews are exclusively authored by our editorial staff, reflecting their own views. These insights remain unswayed by our sponsors. At TheEnquirer, we adhere to stringent principles of editorial independence and fairness to ensure unbiased content..

Expert Verified

Expert Verified

How Does TheEnquirer Ensure Expert-Verified Content?

How Does TheEnquirer Ensure Expert-Verified Content?